Yesterday saw the S&P halt an impressive winning streak, as the index registered a decline of more than 1% for the first time in 95 trading sessions. This not only mirrored weakness already registered elsewhere in the world, but it also triggered Macro Man into his long SPX/short DAX position via the March futures. The knock on effect to risky assets was immediate, with Latin American currencies in particular selling off while Treasuries caught a safe haven bid.

This morning, however, there has been relatively little follow through, and markets await confirmation that yesterday’s sell-off was real. While yesterday’s equity market weakness was superficially similar to some of that observed in late spring, it was actually substantially different. Weakness in May-June was accompanied by bond market weakness and concerns over inflation and Fed tightening. This time around, bonds are at their highs, so further weakness in the absence of a bond market sell-off will be construed as a hard-landing trade. That’s not to say that it won’t happen, as there is plenty of data this week to encourage equity and economy bears if the chips land right. Moreover, after a stunning run, supports have finally been broken (see DAX chart below), which should naturally encourage a bit of profit-taking from longs who participated in much of the summer and autumn rally.

This morning, however, there has been relatively little follow through, and markets await confirmation that yesterday’s sell-off was real. While yesterday’s equity market weakness was superficially similar to some of that observed in late spring, it was actually substantially different. Weakness in May-June was accompanied by bond market weakness and concerns over inflation and Fed tightening. This time around, bonds are at their highs, so further weakness in the absence of a bond market sell-off will be construed as a hard-landing trade. That’s not to say that it won’t happen, as there is plenty of data this week to encourage equity and economy bears if the chips land right. Moreover, after a stunning run, supports have finally been broken (see DAX chart below), which should naturally encourage a bit of profit-taking from longs who participated in much of the summer and autumn rally.

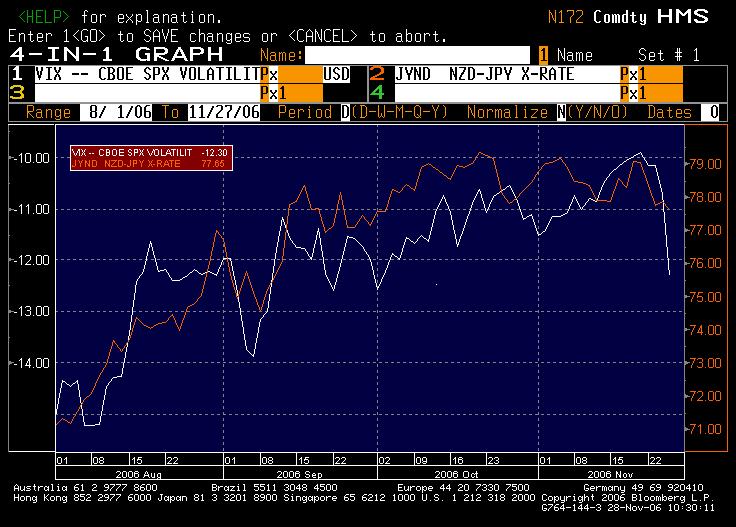

However, this morning has been characterized by the relative resilience of risk assets. The Nikkei and DAX haven’t really moved, and Turkish fixed income and the lira haven’t really sold off, despite the weakness of Latam in late New York. Meanwhile, the NZD, poster child for naked carry and current account risk, has been uber-bid in London. Can this persist? Obviously, anything is possible, and Kiwi strength doesn’t come as a total surprise given the broad-based weakness in the JPY and CHF this morning. However, if the recent rise in equity volatility is maintained, the NZD is almost surely headed for a fall, along with other G10 (and possibly EM) carry trades. A naïve overlay would suggest that NZD/JPY should already be at 76 or lower, rather than the current 78.30!

While it is too early to pull the trigger (we’ll need to see another session of equity weakness/higher vol to confirm the trend), Macro Man is on high alert to sell NZD and go long JPY, CHF, or possibly EUR as and if the carry trade unwind finally becomes a reality.