As vol continues to strangle any substantive macro trends, we’ll get back into the cycle of Economist articles to lead off the week.

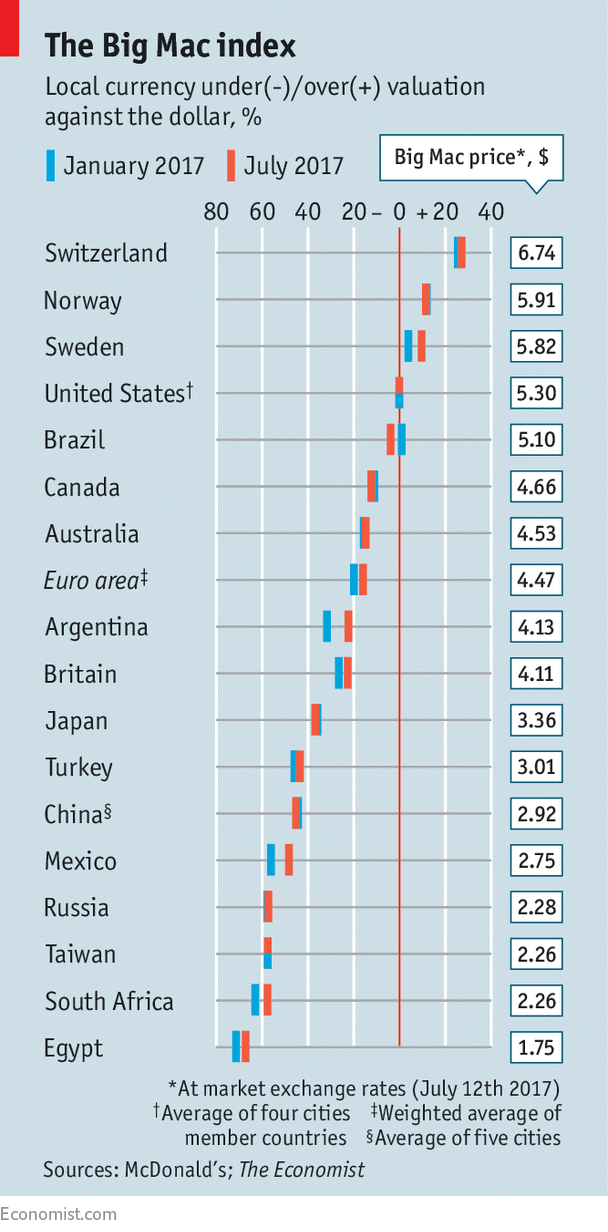

This week’s article for your macro consumption is the annual updating of the Economist Big Mac Index. I must confess to having a soft spot for the Big Mac Index. During my freshman year of college, my intro economics prof introduced the concept to the class. I found it fascinating, and it really connected the dots for what this whole endeavor is about--the quest to find some common “currency” by which we can assign value, or at least give us some evidence by which to make some subjective judgements. For me, it suddenly all made sense. By the end of the year I dropped my plan to be a political science major and the rest is history.

So there you have it--here’s what I see as the takeaways, modest as they might be:

- Sweden still very high on the “overvalued”, and actually appreciating more.

And it’s had a nice run lately, taking EUR/SEK from 9.80 to 9.53--SEK rates have underperformed EUR rates owing to some relatively good data and the potential for the Riksbank to move off of the lower bound of repo rates. That said, 2y2y rate spreads haven’t done much-- if I were to plot this out on a regression the residual is very close to zero.

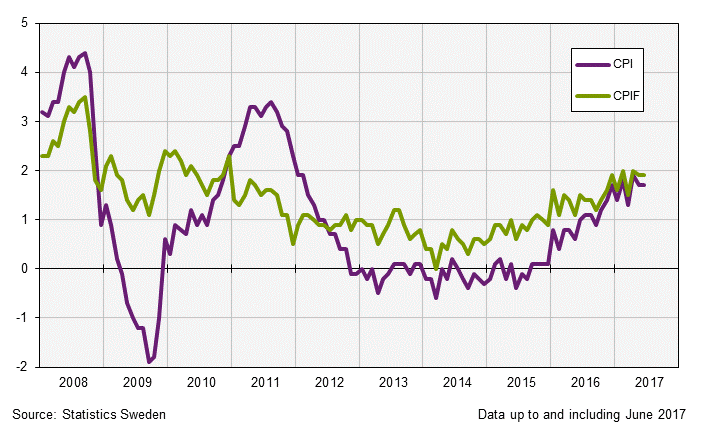

I’ll confess that I haven’t spent a great deal of time thinking about the land of my ancestors--but is there a good argument we’ll see a faster normalization of rates by the Riksbank than the ECB? Unlike with the fed, inflation could arguably be converging towards the 2% target.

Sweden CPI and CPIF (CPI w/ a constant interest rate( source: Statistics Sweden

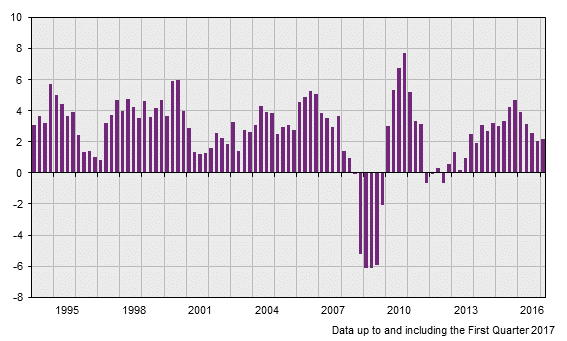

Growth? Not too shabby.

YoY GDP Growth source: Statistics Sweden

Figures for IP look more encouraging--- likely part of the broader trend in the European business cycle. I’d love to hear anyone with a more educated view here, but looks like eur/sek may have gotten a little ahead of itself. Good spot to take a crack at long eur/sek...9.50 looks likely to provide good resistance and an easy point to walk away if it breaks down and/or there is a persuasive move in the forward rate spread.

2) Brazil--BRL has been on a very good run. A very wise friend once told me “when you are bullish, buy BRL. When you are bearish, sell MXN.” Given the political situation in both countries and a convergence in their interest rates, that’s not quite as true as it used to be, but the market sure seems to think so. I continue to like the potential in Brazil, but the politics will continue to be a three-ring-circus--indeed, how many currencies rally when the ex-president is sentenced to almost ten years in prison? Last week I alluded to the Mexican political maxim that “energy reform will be done in darkness.” Well, the metaphorical lights are about to go out in Brasilia...and maybe sooner in Rio. Politicians know what they have to do, they have the goods on the table, and soon they will be forced to do it. Stay long BRL.

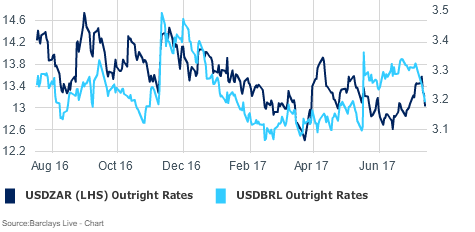

3) ZAR...not as expensive as it used to be--and well, if your answer to the above question was “South Africa”, you would be correct. I think the question is when to get long here--rates are still attractive, and the only institutional respite in the whole country right now is probably the SARB... and you have the wild card option that Zuma is finally sent packing, to retirement, jail, or Zimbabwe...anywhere other than the presidency.

4) Lastly….I know I am fly-over country, but where in the US does a Big Mac cost over $5? Maybe I buy too many Happy Meals to notice? Who would pay $5.30 for a Big Mac when $7 buys you a burger at Five Guys?

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

Update: FRED led me wrong--in the initial version of this post the inflation and growth data I pulled from the normally reliable St. Louis Fed website “FRED” was wrong. I have updated the post to show the correct data, now taken from Statistics Sweden.

5 comments

Click here for commentsWorst flu in years last week, hence the absence despite some great posts.

ReplyRe Shawn's latest, interesting to see SEK over-valued on Big Mac given its under-valuation on so many other measures, e.g. OECD PPP. I'm actually long 6M EURSEK put spreads entered with spot ref=9.75-ish. Sweden's output gap is closed, it's economy is the best post-GFC performer in G10, inflation is close to target and lagged effects of past currency depreciation should support it for awhile yet. On BRL, there's a logic to the rally on Lula's conviction. He polls more than any other potential candidate (around 30%) going into next year's election and he is against pension reform, which is important given Brazil is running a fiscal deficit >8% of GDP. Apparently a higher court will have to uphold the decision to knock him out of the running, and that decision could take a (too) long time. Interesting you view Zuma as an upside catalyst (against a backdrop of a country where real rates are now very high and its central bank likelier to start an easing cycle). Probably right, but I do worry that we'll see investor unfriendly populism in the lead up to ANC leadership and ultimately national elections.

My own thoughts, coming back from the sickbed:

Despite Yellen's remarks about being near neutral (which were actually totally consistent with the logic she outlined in an earlier speech, but which poured cold water on a newly financial conditions driven Fed narrative that GS and Citi among others had recently floated), there's a division between drivers of balance sheet versus rate decisions, with the former driven (almost exclusively?) by growth. So, the QE distortion unwind trade is still on (Draghi probably will try to keep the conflagration down this week, however). There is also the new Euro-zone cohesion story, driven by Macron. He'll be announcing executive orders this summer and probably gets them ratified by parliament this fall. That'll help optimism that Euro-zone integration will take a step forward as a quid pro quo. Whether that happens won't be known for many months, and so optimism has room to grow. My trade that benefits from both is +EURCHF. Seems extended here, so my cash position is small but because EURCHF has been down at the SNB's soft floor until recently, implied vol isn't bad and so I bought calls last week. I also note that UBS saw corporates and private clients selling CHF for the first time in forever just recently.

A couple interesting charts I saw last week: NFIB jobs not able to fill right now, advanced 4 years, versus US productivity growth. It may be that productivity is about to surprise and that will be a shocker for long rates. Maybe all this retail going out of business is going to be one source of thrust to productivity as so much of it is unproductive redundancy in a world with AMZN. Oh, and separate but related, anyone who thinks the next Fed Chair will want low long rates, consider that Trump's voters are old, and the old want and need high rates on fixed income.

Another neat chart was labor hours to buy a share of S&P 500. It's sky high. Millenials are correct NOT to save but buy avocado toast and other "experiences" instead. Saving is a bad deal for Millenials right now, and they'll probably wait until labor income-to-S&P 500 falls closer to levels the Boomers and Silents enjoyed. That doesn't happen until the only big net buyer of US equities post-GFC (as seen in another great chart last week) -- corporates -- stops buying, probably in the next recession, or maybe as was suggested in www.convexitymaven.com if Congress eliminates corporate interest tax deductions.

A final observation. Chinese activity #s were great and Chinese equity markets sold off hard. A chart of the ChiNext is a shocker to anyone who hadn't looked yet this year. Tells you where we are in the cycle there. The market expects liquidity tightening into any economic strength.

Thanks Johno....Re: SEK--A chart I should have added was the BIS REER figures, which no doubt are relatively close to the OECD PPP figures. It shows SEK in the middle of the pack, and never showing too much divergence from EUR (well, not since 2014, anyway). That gets us back to your points on fundamental strength and a faster normalization from the Riksbank than from the ECB. Given the recent move in eur/sek relative to the spread in rates, I'd probably express that theme in rates (pay 2y1y sek vs. eur) rather than FX at these levels--but hey, whatever works....like i said the regression doesn't give you much to work with anyway.

ReplyRe: China...yeah it doesn't look good--we've all been taught to be skeptical of the official data--more important today was the regulators essentially saying there would be continuing tightening of financial conditions. The ball keeps rolling, until it doesn't roll anymore.

Correcting the above, I meant wait until "S&P 500-to-labor income" (not other way as written) falls. Anyone who saw the chart probably knew what I was talking about, while those who didn't might be scratching their heads. Sorry!

ReplyI am with Johno here. SEK appears to me as undervalued looking at various metrics. The Riksbank has done a good job to keep SEK undervalued (specially after a 3-3 vote in December), and considering the shift of tone in the ECB, the Riksbank will soon follow through.

ReplyAn important housing bubble in Sweden is a factor well documented by the Swedish central bank and could be the catalyst for higher rates sooner than expected.

Using some sensitivity analysis, IMHO, it appears - according to my simple models - that higher real rates in the eurozone would not have a very meaningful upside impact in EURSEK, whereas the opposite could send SEK much higher against the single currency

TMM, I'm returning to the QUT macro guesser desk next week so I won't be available for any recommendations for awhile. But I will leave you all with one absolute bird!

ReplyOur desk is BULLISH or OVERWEIGHT, whatever you want to call it, that those media mogul puppy stocks someday down the pipeline square up with the FAKE NEWS rogue publishers big time.

ps.....you might catch me falling out of a drag club