I’m learning to be more blogg-y and less deep dive-y...so a quick blurb on what caught my eye in this week’s Economist. I read it nearly cover-to-cover out at the lake over the long weekend--and while I would love to pontificate on Pakistan and the IMF, the macro story of the week was in the excellent Buttonwood column about the return of easy money.

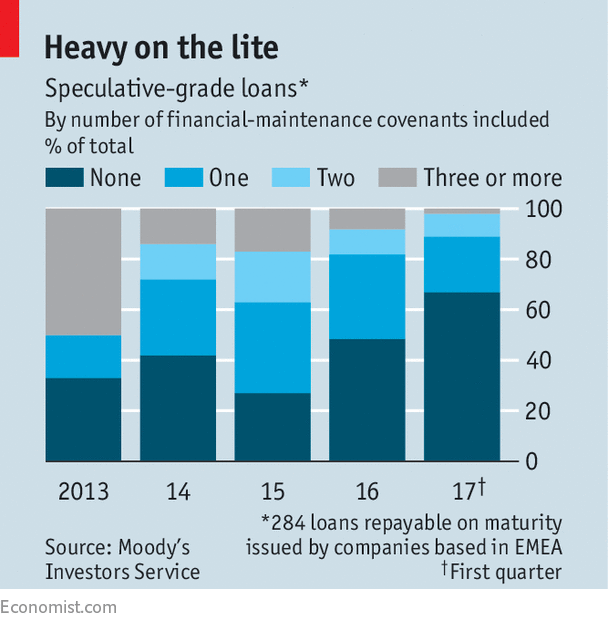

“Analysis by Moody’s shows that the proportion of the loan market that is “covenant-lite” (brilliant that it is the phony “lite” way) has risen from 27% in 2015 to over two-thirds today.”

We know investors are “yield hungry”. But what does that mean? Why are they so hungry?

I wouldn’t ask you to read the investment plan of a standard issue US public pension fund, but if you did, you would read statements like this:

This is about a $70bn fund--with a shortfall of $4bn per year. For round numbers lets call that a shortfall of 6% on AUM per year. The pension fund has a funding ratio of roughly 70%, which is certainly a long way from a margin of safety. Over time, the annual nut to crack is going to get bigger and bigger.

What’s the asset allocation plan that will increase liquidity while closing the funding gap?

| Current | New Target | |

| Cash | 2% | 1% |

| Equities | 65% | 58% |

| Fixed Income | 16% | 21% |

| “Opportunistic/Diversified” | 7% | 10% |

| Real Estate | 10% | 10% |

They need a greater return on assets to plug the funding hole, despite the current level of yields and spreads. But they need safety and liquidity as more and more baby boomers retire. The solution is to move a healthy chunk of dough out of equities and cash and into fixed income.

Drilling into this fixed income bucket, this pension fund is planning to increase exposure to US treasuries in the short-term, the medium-term plan is to reduce UST exposure while increasing the overall fixed income allocation.

What does that mean? Less equity exposure. More non-UST fixed income exposure. More duration. More yield. More cov-lite loans. More risk. Feed me, Seymour.

It is tough to blame the pension fund managers--it’s a sticky wicket. They know the politicians and markets have painted them into a corner. This is the best negotiable solution so long as changes to contributions or benefits are politically radioactive. And if I had to guess, this consultant, along with half a dozen others like them, has given this or similar advice to the vast majority of public US pension funds.

An old Mexican political proverb once said, “Energy reform will be done by candlelight.” While it didn’t turn out to be true of the Mexican energy sector, the metaphor might fit the US pension fund system if credit markets again hit the wall.

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

11 comments

Click here for commentsIndeed, good article that one. I especially thought the penultimate paragraph was good, adds a good viewpoint to the actions of central banks.

ReplyAlso, an eye opener for me was page 62, "The New Old thing" and comment from RBC chap on Apple's price to earnings (top right of page). Changed my perspective of tech actually, at some point with cloud computing etc taking an ever bigger slice of revenues and in the case of apple, established products being renewed, tech companies could trade more from a utilitarian point of view than innovation. [Links in with MM's comments earlier today on NDX levels and sector rotation]

Please don't loose your deep-divey ! Its one of the best features of your blog !

ReplyNice post. Love the deep dives too.

ReplyTotally expecting my tax rate to go through the roof in the 2020's as the pension under-funding gets socialized.

Separately, I was going through my backlog of unread reports and thought these excerpts from a June 28 GS piece interesting given the prevailing views here:

"VIX futures open interest is up 23% over the past year and VIX options open interest is up 20% over the past year. However, net positions in ETPs show that the end investor is actually more “Long volatility” than “Short-volatility”. It seems investors are opportunistically using the decline in implied volatility to initiate long positions in the VIX. We estimate that investors are net Long $60 million Vega (volatility exposure) after considering the positions in all major VIX ETPs.... Admittedly this is less long than normal; this is down from $155m a year ago, and below the 3 year average of $100m."

Given still healthy implied vs realized and net long positioning (admittedly on low side of history shown in charts), maybe still not worth going long. Not my wheelhouse, anyway.

I second keeping the deep dives

ReplyHmm, does GS track net positions including short interest? Many vix etfs are created-to-lend, and there's a substantial otc element. E.g. About 1/4 of all VIX options trade as otc lookalikes, for instance, given the cboe's high on-exchange fees.

ReplyStill, a lot of reflexivity in the product, given the number of SPX strategies risking to realized vol in SPX these days and the money flow into short vol strategies by pensions (Canadians have done for twenty years, Americans just joining the bandwagon. Political pension board appointees, sigh.)

Levered etp net vega outstanding (which will be forced into rebalancing end of day in a nonlinear way, on any spike) is near all time highs, one of the reason why the implied of the options on VIX is elevated (vs what you might expect given the level of vix futures)... Basically, vvix vs vix, expect end of day fireworks in particular, a grand finale, on any big move intraday .

Holding a few months out might ease the pain of decay, though there's probably some good relative value too.

thanks for the feedback there--I used to read a lot of sell side research that recycled the news and didn't dig beneath the surface. I think it was an editorial decision--the long stuff just doesn't get read! Or is kept as proprietary for the prop desk or big clients, if you are conspiracy-minded. Worry not, I'll mix it up so there is some quick thought provoking clips along with the long-form.

ReplyRe: vix futures--I remember years ago, i don't recall exactly when--a PM at my fund was long "vol of vol", which at the time sounded patently ridiculous as a concept. I don't think it worked out for him. I never know quite what to make of the type of analysis from the GS piece--I'm sure it is important if you are a VIX futures trader in my experience you don't know if that kind of thing is the catalyst for a broader market move until the post mortem.

@ Rain, glad to know I'm not the only one that still reads the print version!! I did read that Apple piece at the lake--they kinda lost me with the "augmented reality" stuff--but it did occur to me that most companies are really terrible at "change". Even tech companies. Maybe Apple will prove to be different--I would grant Tim Cook that the P/E has traded cheap for years now but the stock price keeps going up. But history would argue it is impossible for such a large company to innovate itself out of traditional high margin businesses. Time will tell. For sure Tim Cook is kicking himself for not striking gold with content like Netflix did.

@ universal portfolio, thanks for the reminder on pension funds getting involved in short vol strats--i forget where I read that previously-- that is part of what is in the diversified/opportunistic bucket that is increasing from 7% to 10% in the pension fund I mentioned above. They call it "volatility risk premium".

ReplyActually I would have thought it nigh impossible to put a significant dent in the shortfall by increasing exposure to UST. Indeed I would have thought ,comment notwithstanding, that to do so they intended to fish further down the bond risk spectrum than they currently do which is what many non pension players have now been doing for some years.

ReplyOf course the moment pension players essentially start taking on more risk is when Murphys Law will kick in.

The underlying concept is true enough that the low rate enviroment is playing havoc with pension funding on every level from National right down to the aging individual pension contributor. God knows how that plays how at the end of this cycle if rates are still very low and we enter a new economic downturn.

For the past I dunno 10-20 years we have had rising asset values (ie multiples, cap rates etc) as the tail wind to keep underfunded pensions (and municipals) in order. But thats about done (not withstanding a possible test for US rates at the zero bound come the next recession). It will be a lot easier to inflate than to get pensioners to delay retirements for a few years (which would be a very practical solution to most of the underfunded mess, just increase the age to 67 or 68). My guess is a return of inflation (above what funds are indexed to) plays some sort of role.

ReplyNice post

@ checkmate, yes you're absolutely right--this fund is increasing absolute exposure to UST, but it is a transitional move before rotating into more yield, risk, duration, etc.

Reply