To those in the US, welcome back from the most American of holidays. I’m sure there are other countries that have holidays largely devoted to gluttony, but as is often the case, America imported a good thing and made it better. Well, bigger and more gluttonous, anyway. Who else would have woven in nine hours of football and materialist retail bonanza into a celebratory feast day? Heck, now you don’t even have to drive to a retailer at sunrise and risk getting trampled to death to grab the best Black Friday deals. You can do it while sitting on the couch! Well done, America. U-S-A! U-S-A!

I’m back at my desk after a travelling for a couple of weeks and spending much of last week considering, buying and preparing my contributions to the Thanksgiving Day feast. The big story of the past two weeks has been the re-pricing of the front end of the curve in the US:

You don’t get a 30bp move in the 2y with the the 10y pinned in a 10bp range over a six week period without considering the message the market is sending to the Fed. Clearly there isn't much cooking in term premiums....the market hasn't lost faith in the lower natural rate, r*, or whatever you want to call it.

Which leaves us with this move in the front end, and what it all means. Please use the comment section to tell me what you think the market's message is...my two contributions would be 1) “there’s still a ton of liquidity out here”, and 2) “we don’t think the business cycle is sustainable, nor do we believe core inflation dynamics are going anywhere.”

Before this slips into another “curve shape” post, it is the second message I want to focus on. While there has been little evidence that “demand-push” inflation is outside what we might expect at this stage of the business cycle, the buried message is related to big increases in oil, gas, and fuel oil prices since early this summer. As much as they will tell you these prices are “transient” and thus don’t impact monetary policy, they will likely be tough to ignore in 2018 because they will hit consumers in the pocketbook and push headline inflation higher.

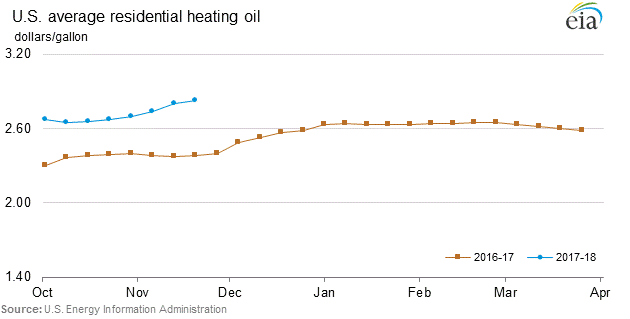

We all know what the crude chart looks like, with the move from the low 40s to the mid-high 50s in WTI, roughly a 30% move. There has been a similar move in residential heating oil:

And as we come into the heating season, prices are tracking well above last year:

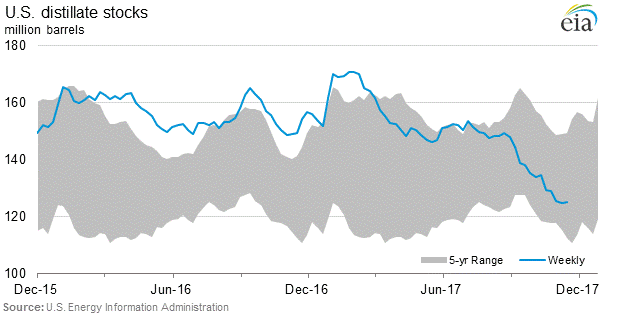

And inventories are approaching 5-year lows, which argues for big prices increases if we get a cold winter (that being said, I’m planning on running outside in a t-shirt today).

There have been similar price increases throughout the energy complex--gasoline tends to grab the headlines, and has been somewhat spared--but the marginal increase in global demand in 2017 has been the big story, and the impact on headline inflation is likely to show up in early 2018 just as the Fed is wrestling with what to do next. At the very least, these price increases have to play a role in the December Summary Economic Projections...the dots.

The FOMC will have a tough time justifying headline inflation projections aren’t rising, and they have a preternatural desire to write off energy-driven inflation as a transitory factor. But time and again energy is the tipping point for changes in the speed of the economy. It will be acting as a brake here...leading to the flattening of the curve. That combination has painted the Fed into a corner. Do they have the guts to continuing hiking if the economy is doing well, headline inflation is pushing higher, but core continues to lag behind?

It seems like the answer is yes...can they get away with four hikes in 2018? If so, 2x10s is going to zero….

Absent a big move in core, what can change the demand for duration in the long end? Can this chart steepen the curve?

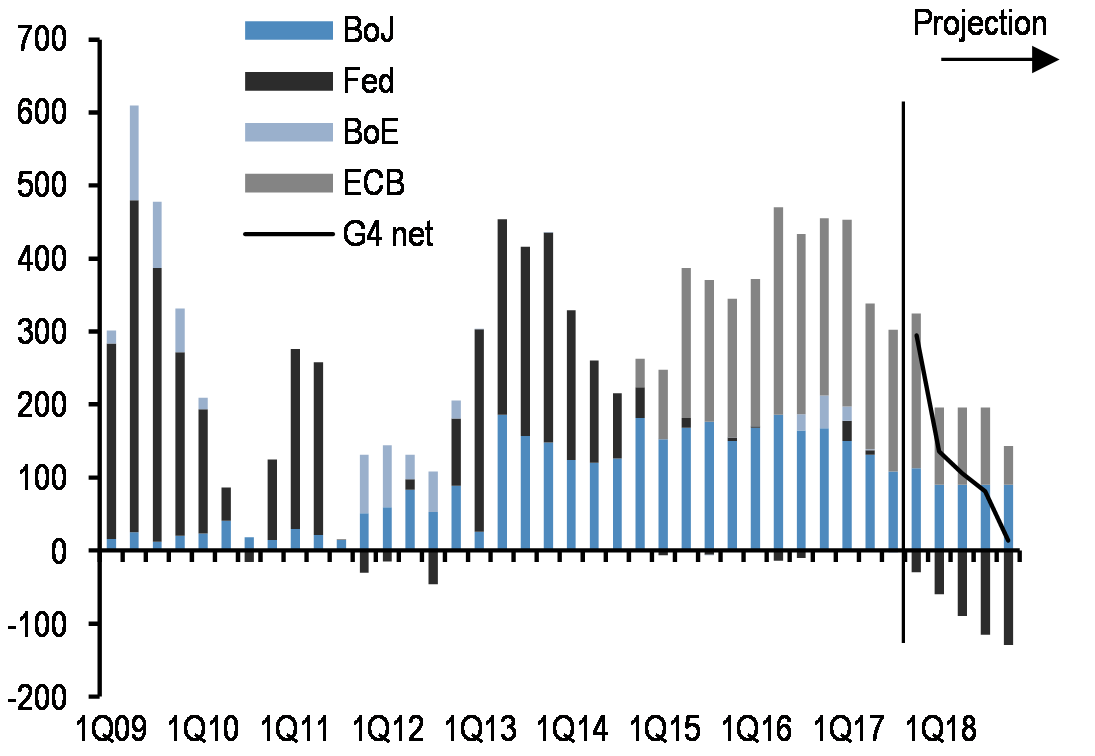

Or will US tax reform put a supply-side kick in the long-end? Supply doesn’t matter...until it matters. There will need to be a catalyst to change the narrative for buyers of duration...the demand side. I can’t see what it can be other than core inflation--probably on a global scale. While I continue to believe measures I have discussed in the past like the NY Fed’s underlying inflation gauge show there is price pressure in the economy, the market just won’t believe it until it really gets out of hand and forces the hand of not just the Fed, but of the ECB, BoJ, and even the PBoC.

Until then, the only thing out of hand is this flattening trend. And bitcoin.

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

Shawn

TeamMacroMan2@gmail.com

@EMInflationista

191 comments

Click here for comments"In the past 40 years, it has typically taken 7 months for the yield curve to go from flat to inverted and then another 14 months for a recession to begin. On its own, a flattening yield curve is not an imminent threat to US equities. Under similar circumstances over the past 40 years, the S&P has continued to rise and a recession has been a year or more in the future." -- Urban Carmel, from today's The Fat Pitch post

Replyhttp://fat-pitch.blogspot.com/2017/11/the-flattening-yield-curve-is-not.html

Agree the curve is no objection to being long stocks here, Gus. Otherwise not sure there's much to take from it other than market is fixed in its low neutral rate view. Actually, my guess is the the curve continues flattening until short rates are close to long, at which point short rates will drag up long. That's what happened in the last cycle and it makes some sense. Long end will want to see steady inflation around 2% before it goes much higher, and Fed Funds are only getting to 2% if inflation gets there (the blueprint Yellen layed out some time ago was to get to 0% real when inflation got to target).

ReplyMost notable piece of news today, IMO, was the Reuters sources story saying China likely to keep 6.5% target in 2018. Otherwise, the German SPD coalition news and the Dec 4 deadline for a Brexit offer.

I dunno about all stocks going up though. Financials need a steeper curve and are going to be upset about 2s10s taking a trip to an IHOP.

ReplySpecifically, KRE is looking very toppy here. I still see it going down to backtest d/tops @ $46.

Your 1 & 2 are basically what I said to LB weeks ago in the case of do you trust the govt bond market to be a reliable judge of economic outlooks. I also suspect that bond markets would view the impact of energy on inflation to be less a cause for concern as they probably think energy sector up equates to sectors like clothing et al to be down as disposable incomes take the hit. So energy up is retail down ?

ReplyOther than that I'm with Gus post that yield curves are a test of patience for timing purposes. There again my portfolio is never a one or the other 'bet'.

Joining the dots of that previous post the one issue that breaks the bond market reasoning is if aggregate disposable incomes get the kind of uplift that makes price pass through a real inflation threat. That would bring us back to the two issues of tax policy and data on increases in earnings.

Replyyes, my point is that energy inflation (beyond just what we pay for gas at the pump) is going to cause the fed to roll out the "transient" excuses again and test their commitment to hike in the face of higher headline figures despite lagging core inflation.

ReplyOn the broader point, I don't think there is a causative relationship between the performance of the economy (or stocks) and the shape of the curve, except in the most extreme steepening cases (and to financials). I guess the curve shape isn't too far disconnected from what the Fed has been telling us about long-term interest rates, which is perhaps the most telling difference in this cycle compared to previous ones. Far shallower....but no shortage of financial excess.

Re: energy up/retail down theme, I'd say too much going on in retail to bet on that correlation, although from here I'd tend to agree with the idea.

If you are unsure of what the bond traders are telling us, check out what the Dr Copper traders are telling us. Copper is off approx 5% from yearly highs and currently at the lower end of a channel on the weekly. One of them will give the answer.

ReplyThere used to be a really good underlying rational for following the message of DR Copper. Not sure it's quite as applicable today. Maybe Madame Polyurethane as introduced a certain technological change to the issue.

ReplySo 2014 the oil price fall leads to curve flattening and the 2017 oil price rise leads to curve flattening as well?

Reply@Rob...yes! 2014-2016, global repricing of energy (and most commodities), EM stress, UST FTQ, wider credit spreads, fed on hold, lower for longer. bull flattening.

Reply2017: higher global growth expectations, dramatically tighter credit spreads, still abundant liquidity, core inflation still in the gutter but FOMC hiking to offset easier financial conditions and expected uptick in core dynamics. Bear Flattening.

All that said, your point is a valid one, it does sound ridiculous and unsustainable. The more salient driver of the flattening trend stretches across both time frames and is summed up nicely in this presentation from Bullard a couple of weeks ago.

https://www.fedinprint.org/items/fedlps/293.html

GBP interesting, no? If markets can assume status quo for some years after Brexit, what you're left with is an economy with a central bank in motion, its inflation forecasts above target through the whole forecast period, and full-employment. A simple regression on 2Y spreads vs G10 since 2000 shows big undervaluation. Interesting setup ... got long recently through options but added some delta one exposure today on the Telegraph article. We'll see ...

ReplyOh my God, you lot are stupid beyond belief! Forget all this "macro" sh*t (which doesn't work). If you want to produce real Alpha you just buy stocks in size. SPX is going to double from here before we get a 50% re-trace, so I suggest you go long SPX (with as much leverage as your worthless risk managers will allow). You can thank me when you're retired next year.

Reply@BS, not sure why you assume that we don't own stocks. Most of us do. So your repetitive message of decrying us, "stupids", is inappropriate at best and quite offensive at worst. If you are so keen on teaching us how to do our work, why don't you give us five stocks which will outperform SPX for the next year and come back here on Nov 28 of 2018 to size up? Simply telling us to go long SPX and hold it until it doubles is like teaching us to get out of bed every morning. You come across as an arrogant SOB. Here are two things we would thank you for right now: shutting the f*ck up and leaving us alone.

ReplyNow, excuse me as I continue to vent about a more important issue... What is this crazy idea of raising taxes back up if the economic growth slows? I get the whole reasoning coming from the deficit hawks, but it is so flawed. One has to wonder if Cohn and Mnuchin were arm-wrestled by DJT to sign off on this nonsense in order to simply have the Senate pass the bill, any bill. Let me see... We are cutting taxes to stimulate growth but will raise them back up in the event the projected growth target is not attained. Say what?!! You don't raise taxes when economic growth slows as you will further hinder such to a point of generating even lower tax revenues. Even a fifth grader knows this.

Wow, easy there IPA...the year is almost over. I wasn't sure how much sarcasm there was in that comment so I held my fire, but I was going to say the buy SPX rant was amateur level trolling and that we really have higher standards and expectations around here. does amps have a seminar or a slide deck on this kind of thing?

ReplyDamn the crew is getting froggy in this thread...shittt son. Before I post my thoughts I gotta say @Shawn ur line asking if AMPS has a slide deck on this kind of thing is fucking hilarious. God I love that guy, he’s gonna come hard in the paint on you for that one!!!...@IPA come on u know that’s funny...I haven’t read the entire thread yet so I’m not trying to stir shit up...but that’s for real straight funny.

ReplySorry, guys... I come here to exchange ideas, learn new things, brainstorm, listen to others with bright minds, all in pursuit of keeping sane in the world where brainless people are allowed to lead the masses. The last thing I need is one of these degenerates to repeatedly tell me how to "produce real Alpha" by going long the actual index I am supposed to beat. It's an oxymoron! Or is it simply a moron?

ReplyJust giving you a hard time brother...I feel u. Long the $SPX isn’t that the Grandpa Buffett call these days? I couldn’t look the investors (family office) in the face and give them a mgmt fee. More than .25 or less if that’s all I did. Same w our advsing firm man.

Reply'sorry guys' really ?

ReplyI have to tell you these days I feel like I live in a world that is arse backwards. It seems the thing is to apologise for having a bad thought about anyone or anything. I don't get it. If a wanker wants to get into your life tell the fucker to crawl back into his hole and leave it that. He's free to do whatever he likes about it ,but the main thing is don't hand the twat a free license to think you'll just let him. Behaviour should have consequences and I don't mean apologies where none are required.

It's getting really insane out there.

ReplyLet's try to keep our wits about us and stay cool, calm and collected.

LB is inclined to fade today's moves in USDJPY and rates. That GDP revision is/was old news.

Rear view mirror investing never works out well.

CBs are going to want to burst the bitcoin bubble, trust me on this, it's classic tulip bulb stuff.

The question is what else will they bring down in the process of letting out some hot air?

Any views on likelihood of Irish border blowing up talks in the final stretch here?

ReplyThese banks saying pound has no upside from here if we move to the transition talks are full of it, IMO. Question is how aggressive to get ... which hinges on Irish question now. Big in options and delta one, but former has me nervous ...

Oh, 10Y gilt futures are sell if you believe these r* estimators ... the annoying thing is they don't trade 24-hours, which is a strike against for small punters like me.

Bitcoin going past 10k to 11k reminds me of Spinal Tap. Turn it up all the way, Nigel.

ReplyA big reversal candle is forming in the NAZ. I suspect it will not be the last one this week.

Note that a stronger USD is now no longer automatically good for risky assets.

FX regime change afoot? If so, usually indicative of major infection points/turns in the markets.

If the USD and JPY start to rally together, the 12 y-o punters need to look out below.

Meant latter ...

ReplyAnyway, views welcome.

Momos are offered.

ReplyFB down 4%, NFLX off 6%. Fun.

The vol selling ETFs are off 3%.

We are synthetically long vol, via the short VIX universe.

Things could get messy for Chad, Brad and Thad.

:-)

ok, ok....sorry i threw some gas on the fire there. My apologies.

Reply@leftback, per your point on USD, I read over the weekend that the quant guys at JPM have flipped the sign on the correlation of USD to inflation....stronger USD now implies higher inflation, because of capital flows, risk on, etc. etc.--they argue this impact is now stronger than that of lower import prices. Maybe not worth the paper (or electrons) it was printed on, but worth a thought.

Another piece by Peter Tchir on the perils of vol selling, consequences that might extend beyond the VIX complex itself:

Replyhttps://www.forbes.com/sites/petertchir/2017/11/27/renaming-vix-the-greed-gauge/#767182ad7552

Thank you for the posts. This article is very useful.

ReplyThank you very much.

ท่องเที่ยวจังหวัดอุบล

ร้านอาหารต่างประเทศ

ฮวงจุ้ย

Thank you for the posts. This article is very useful.

ReplyThank you very much.

รีวิวตัวละคร Leeague of legends

ขนมมงคล

ทะเลไทยไม่แพ้ชาติใดในโลก

ฉันชอบบทความของคุณ

Replygoldenslot

สล็อตออนไลน์

สมัคร gclub

คาสิโนออนไลน์

maxbet

m8bet

ReplyThanks for a great article. :D

วิธีีทำเค้ก

ดาราเกาหลี

แหล่งรวมซีรี่ย์

Thanks for sharing it.

Replyสุขภาพและเทรนด์

พันธุ์สุนัข

วิธีลดความอ้วนโดยไม่เสียเงิน

ReplyThanks for a great article. :D

ออกกำลังกาย

ตำนานผีไทย

ตำนานเรื่องเล่าต่างๆ

ขอบคุณสำหรพับการแชร์ข้อมูล

Replym8bet

แทงบอลออนไลน์

sbobet mobile

royal1688

ทางเข้า sbobet

Thank you.

Replyนอนไม่หลับ

dtogenthailand.com/Insomnia

หนังโป๊ไทย yagyed.com

Replyคลิปโป๊ heedum.com

รูปโป๊ asiannudepic.com

คลิปหลุด heehiso.com

หนังโป๊HD porn4k yagdu.com

Most notable piece of news today, IMO, was the Reuters sources story saying China likely to keep 6.5% target in 2018. Otherwise, the German SPD coalition news and the Dec 4 deadline for a Brexit offer.

Replyแทงบอลออนไลน์

ข่าวกีฬา

Thanks for your sharing

Replyฟีฟ่า55

สโบเบ็ต

gclub มือถือ

baccarat

Note that a stronger USD is now no longer automatically good for risky

Replyิbet365

Replyhank you for the posts.

ufa88

Thank you for the posts

Replyเทียบราคาบอล

I like your article.

Replyิbet365

Most notable piece of news today,

Replywww.ufabet.com

Games that have played fun. เครดิตฟรี ไม่ต้องฝาก

ReplyMost notable piece of news today,

Replyพนันออนไลน์ เว็บไหนดี

Most notable piece of news today,

Replyคาสิโนออนไลน์

Most notable piece of news today,

Replyfun888

Thank you for the posts

ReplyUFABET

Thanks for the rare information. And very useful. ข่าวบอลไทย

ReplyThis information is very helpful.

Replyรักบอล

very helpful.

ReplyUFABET ราคาบอล

สมัครเล่นบาคาร่าออนไลน์

Replyสมัครเล่นบาคาร่าออนไลน์

สมัครเล่นบาคาร่าออนไลน์

Thank you for the posts

Replyวิธีสมัครเว็บพนันบอล

posts

Replyพนันบอลออนไลน์ ฟรี

Want to have money to use, don't run out, click now !! เว็บแทงบอล

ReplyMost notable piece

Replyวิธีเลือกเว็บ UFABET

Thank you for the posts

Replyวิธีเลือกเว็บ UFABET

Thank you

Replyเว็บแทงบอล ที่ดีที่สุด

Want to have money to use,

Replyเว็บแทงบอล ต่างประเทศ

don't run out,

Replyเว็บแทงบอล ฟรี

Most notable piece

Replyเว็บแทงบอล ดีที่สุด

UFABET เว็บแทงบอลที่ดีที่สุด

Replyแทงบอล

ReplyWant to have money to use,

Replyเว็บแทงบอล ดีที่สุด

Want to have money to use

Replyแทงบอลเครดิตฟรี

thank you for the great information by casino55asia.com

ReplyThanks for the good information I gangnamclinicth.com will keep following your article.

ReplyThank you for sharing. UFABET แจกเครดิตทุกวัน

Replyข่าวบันเทิง วันนี้ ล่าสุด

Very good information I peterwindowfilms.com will follow your next article.

ReplyThank you for sharing

Replyแทงบอลสเต็ป UFABET

Thank you for sharing

Replyแทงบอลมือถือ

Agree the curve is no objection to being long stocks here, Gus. Otherwise not sure there's much to take from it other than market is fixed in its low neutral rate Recommend website casino

Replyคลิปหลุดน้องจูน

Replyน้องจูนเป็นสาวนักเรียนมอต้นหน้าตาน่ารัก น้องเป็นคนชอบเล่นโซเชียลแล้วอยากได้รายได้พิเศษ เลยโพสหางานในเน็ต

แต่มันมีพวกหื่นทักไปหาน้องจูนแล้วบอกว่ามีงานให้ทำ รายได้ดีมากแถมสะบายทำอยู่ที่บ้านได้เลย โดยพวกนี้จะใช้เงินล่อ

โดยการขอเลยบัญชีน้องจูนแล้วโอนไปให้ก่อนหลอกให้ตายใจ แล้วให้น้องถอดเสื้อผ้า ไลฟ์สดxxxโชว์แล้วเอาคลิปโป๊ที่แคปไว้

เอาไปขายในกลุ่มลับและเอาไปโพสตามเว็บโป๊ต่างๆ น้องๆที่อ่านก็ต้องระวังกันด้วยไม่งั้นอากจะมี คลิปโป๊ เหมือนน้องจูนออกมา

thank you

Replyแทงบาคาร่ากับ UFABET

เยี่ยม . เล่น คา สิ โน ออนไลน์ ให้ ได้ เงิน

Replythank you

Replyผลบอล

Oh my God, you lot are stupid beyond belief! Forget all this "macro" sh*t (which doesn't work). If you want to produce real Alpha you just buy stocks in size. SPX is going to double from here before we get a 50% re-trace, so I suggest you go long SPX (with as much leverage as your worthless risk managers will allow). You can thank me when you're retired next year.

Replyไฮไลท์บอล

thank you have a nice days

Replyเสื้อผ้า ลดราคา

thank you have a nice days

Replyผลบอล

thx!

Replyเลขเด็ด ดูดวง

thank you

Replyปิแอร์-เอเมอริค โอบาเมยอง

thanks. ศิลปิน นักร้อง

Replythank you

Replyศิลปิน นักร้อง

Review Gadget

Replythank you ตำนาน แมน ยู

ReplyI Love You . Thank you

Replyกันเนอร์

หนัง hd

โต๊ะบอล UFABET

Thanks for your sharing

Replyเลขเด็ด

Thank you

Replyดาราหญิง

Thank you

Replyข่าว

Thank you .

Replyปิแอร์-เอเมอริค โอบาเมยอง

หนัง hd

แทงบอลมือถือ

nice post.ดาราหญิง

ReplyThank you .

Replyเน็ตไอดอล

thanks ข่าวลิเวอร์พูลสยาม

Replygood post man thank you เสื้อผ้า ลดราคา

ReplyThank you

Replyข่าว อาร์เซน่อล

หนัง hd

แทงบอลสูงต่ำ

Thank you

Replyข่าวด่วน

nice post.เน็ตไอดอล

ReplyThank you

Replyข่าวบันเทิง

thank you

Replyไฮไลท์ฟุตบอล ลิเวอร์พูล ล่าสุด

ดูหนัง hd

แทงบาคาร่าที่ UFABET

เลขเด็ด

Replyส่วนลด amazon

Replypizza company ซื้อ 1 แถม 1

สเวนเซ่นส์ เมนู

พิซซ่า คอมปะนี 1แถม1 2562

oishi eaterium สาขา

เฟอร์นิเจอร์ index ลดราคา

noksmilebooking

1112 ออนไลน์

oishi buffet สยาม

ชุด kfc 199

สั่ง พิซซ่า ออนไลน์ 1 แถม 1

oishi grand promotion

โออิชิ บุฟเฟ่ต์ โปรโมชั่น 2019

7-11 ลดอย่างแรง

hotpot โปรโมชั่น

ราคา ฮอด พอ ด

look gorgeous! ข่าวเกม | เกมฮิต

ReplyThanks for sharing

Replyคนบ้าหวย

ข่าวกีฬา

ข่าวกีฬา

อาร์เซน่อล

Thanks for your sharing

Replyหวยเด็ด

คนบ้าหวย

อาร์เซน่อล

มือถือเล่นเกม

thank you

Replyเลขเด็ด

ข่าวกีฬาวันนี้

ข่าวบันเทิง

pizza company ซื้อ 1 แถม 1

ผลบอลเมื่อคืนนี้

ฟุตบอลต่างประเทศ

ฟุตบอลต่างประเทศ

Thank you for your info , Good Blogger

ReplyMovie2FreeYou.Com

ดูหนังออนไลน์ 2020

ดูหนังออนไลน์ฟรี

wellcome to may website

Replysexybacara

wellcome to my website

Replyufabet365

wellcome to my website

Replyufabet365

https://bignameking.page.tl/%26%233618%3B%26%233641%3B%26%233648%3B%26%233609%3B%26%233637%3B%26%233656%3B%26%233618%3B%26%233609%3B-%26%233648%3B%26%233610%3B%26%233629%3B%26%233619%3B%26%233660%3B%26%233621%3B%26%233636%3B%26%233609%3B%26%233610%3B%26%233640%3B%26%233585%3B%26%233648%3B%26%233594%3B%26%233639%3B%26%233629%3B%26%233604%3B-%26%233652%3B%26%233629%3B%26%233609%3B%26%233660%3B%26%233607%3B%26%233619%3B%26%233633%3B%26%233588%3B-%26%233649%3B%26%233615%3B%26%233619%3B%26%233657%3B%26%233591%3B%26%233588%3B%26%233660%3B%26%233648%3B%26%233615%3B%26%233636%3B%26%233619%3B%26%233660%3B%26%233605%3B-%26%233588%3B%26%233634%3B%26%233610%3B%26%233657%3B%26%233634%3B%26%233609%3B-2_1-%26%233651%3B%26%233609%3B%26%233624%3B%26%233638%3B%26%233585%3B%26%233610%3B%26%233640%3B%26%233609%3B%26%233648%3B%26%233604%3B%26%233626%3B%26%233621%3B%26%233637%3B%26%233585%3B%26%233634%3B-%26%233648%3B%26%233618%3B%26%233629%3B%26%233619%3B%26%233617%3B%26%233633%3B%26%233609%3B.htm

Replyhttps://medium.com/@bignameking/%E0%B9%82%E0%B8%A1%E0%B8%AE%E0%B8%B2%E0%B9%80%E0%B8%AB%E0%B8%A1%E0%B9%87%E0%B8%94%E0%B8%8B%E0%B8%B2%E0%B8%A5%E0%B8%B2%E0%B8%AB%E0%B9%8C-%E0%B8%9C%E0%B8%B9%E0%B9%89%E0%B8%97%E0%B8%B5%E0%B9%88%E0%B8%97%E0%B8%B3%E0%B8%9B%E0%B8%A3%E0%B8%B0%E0%B8%95%E0%B8%B9-15-%E0%B8%9B%E0%B8%A3%E0%B8%B0%E0%B8%95%E0%B8%B9-d48fd1c800e6

https://sportoioi.blogspot.com/2020/02/4-4-1-3-3-3-3-mmm-17-7-36.html

https://bignameking.wixsite.com/meinewebsite/post/%E0%B9%80%E0%B8%9C%E0%B8%A2-%E0%B8%9B%E0%B8%AD%E0%B8%A5-%E0%B8%9B-%E0%B8%AD%E0%B8%81-%E0%B8%81%E0%B8%AD%E0%B8%87%E0%B8%81%E0%B8%A5%E0%B8%B2%E0%B8%87-%E0%B9%81%E0%B8%A1%E0%B8%99%E0%B9%80%E0%B8%8A%E0%B8%AA%E0%B9%80%E0%B8%95%E0%B8%AD%E0%B8%A3-%E0%B8%A2-%E0%B9%84%E0%B8%99%E0%B9%80%E0%B8%95-%E0%B8%94-%E0%B8%A2%E0%B8%AD%E0%B8%A1%E0%B8%A3-%E0%B8%9A%E0%B8%A7-%E0%B8%B2%E0%B9%84%E0%B8%A1-%E0%B8%AD%E0%B8%A2%E0%B8%B2%E0%B8%81%E0%B9%80%E0%B8%AB-%E0%B8%99-%E0%B8%A5-%E0%B9%80%E0%B8%A7%E0%B8%AD%E0%B8%A3-%E0%B8%9E-%E0%B8%A5-%E0%B8%84%E0%B8%A7-%E0%B8%B2%E0%B9%81%E0%B8%8A%E0%B8%A1%E0%B8%9B-%E0%B8%9E%E0%B8%A3-%E0%B9%80%E0%B8%A1-%E0%B8%A2%E0%B8%A3-%E0%B8%A5-%E0%B8%81

https://justking.food.blog/2020/02/25/%e0%b8%9e%e0%b8%a3%e0%b9%89%e0%b8%ad%e0%b8%a1%e0%b8%97%e0%b8%b5%e0%b9%88%e0%b8%88%e0%b8%b0%e0%b9%80%e0%b8%aa%e0%b8%b5%e0%b8%a2-mako-vunipola-%e0%b9%83%e0%b8%99%e0%b8%95%e0%b8%ad%e0%b8%99%e0%b8%99/

Replypage

Replymedium

sportoioi

wixsite

food

Your articles are extremely useful for daily life. Helps me to have more knowledge

Replysddthdf.post-blogs.com

You do great We appreciate your ability to do this great. Click

ReplyGreat post but I was wondering if you could write a little more on this subject? I’d be very thankful if you could elaborate a little bit further. Thanks in advance! Interested in playing games for real money. Click >>> fhbdgf.blogerus.com

ReplyThank you for sharing information. It's a great post. Interested in playing games for real money here.>>>kjuik.blogprodesign.com

ReplyThank you for sharing information. It's a great post. Interested in playing games for real money here

Replymanop29.ambien-blog.com

ReplyThe blog that you follow is very useful to me and others. If going to play a fun game and real money, click >>>

fvsrdrgg.csublogs.com

Thank you for sharing information. It's a great post. Interested in playing games for real money heremanop1.bloggerswise.com

ReplyGood message.

ReplyPlease follow the website.

manop2.blogzet.com

Great post but I was wondering if you could write a little more on this subject? I’d be very thankful if you could elaborate a little bit further. Thanks in advance! Interested in playing games for real money. Click >>>

Replymanop3.blogpostie.com

Pep Guardiola

Replyhoro271287362.wordpress.com

Reply

ReplyI like your article very much. If you are interested in playing games and making good money too

rygfdgv.blogprodesign.com

ReplyThanks for allowing me to view this portal which is full of relevant knowledge. We have reviewed the information provided and can claim that this is quite authenticated and we would recommend this to our friends. Surely we would also like to introduce ourself as HND Assignment help with below set of relevant websites:

5e6891411e00d.site123.me

This is a very good article, so I will not miss reading it, so I can get insight. And Here we will share information about tips on harmony with couples in a family >>>

Replymedium.com

I loved this blog post. It was practical. Keep on posting Click here >> chelsea

ReplyHi there, just wanted to say, I loved this blog post.

ReplyIt was practical. Keep on posting!

"siam lotto

"

Thanks for the great article. Click here to read my stuff Click >> ทีเด็ด

Replyเว็บดูซีรี่ย์ออนไลน์เพื่อความบันเทิงผ่อนคลายจากการทำงาน แนะนำเว็บ เว็บดูซีรี่ย์ออนไลน์

Replyi99MAX.COM เว็บอันดับหนึ่ง เว็บพนันออนไลน์ครบวงจร ที่เน้นเอาใจคนไทยมากที่สุด ราคาดีที่สุด วิธีเล่นหลากหลายที่สุด จ่ายเงินตรง ฝาก-ถอนเร็วมากที่สุด!!!

Replyi99

i99max

แทงบอล

บอลออนไลน์

แทงบาคาร่า

พนันออนไลน์

เว็บบอล

ดูหนังออนไลน์||หนัง||หนังออนไลน์||ดูหนังออนไลน์ฟรี||หนังใหม่||หนังซูม||หนังภาคไทย||หนังเต็มเรื่อง||ดาวโหลดหนังฟรี||ดูหนังฟรี||เว็บหนัง||หนังฟรี||หนัง77

Replyjust wanted to say

ReplySBOBET ถอน

https://sbosportclub.com/

thank you for watching

ReplyWwwsbo

ข่าวเกม

Replyข่าวมือถือ

ข่าวไอที

ReplyThe information you provided is very interesting. Thank you for the hardships.. Sexy Baccarat

kfcconsole

Replyhttp://ufa345gold.com/

Reply7m

The information you provided is very interesting. Thank you for the hardships.. ความเป็นมาของสล็อต

Replyconvert aud to inr free exchange rate currency tool https://aud.toinr.today

Replybest restaurants in the world https://best-restaurant.co

convert kwd to inr free exchange rate currency tool https://kwd.toinr.today

pubg mobile in arabic https://pubgmobilepc.net

Nice Information! I personally really appreciate your article. This is a great website. I will make sure that I stop back again. These are some really great tips! Another important note is to make sure you give completely specific instructions to your cleaning staffs.

ReplyThanks,แทงหวยออนไลน์

https://fun88club.net/

https://zaza000.hatenablog.com/

https://188betgroup.com/

Want to know what this website is? If you want to know, click on it.slot online Richness awaits you. http://v9betonline.com/ | https://daymanjesus.hatenablog.com/

ReplyI want to try to come in and read new articles because it is a knowledge base. วิธีแทงบอลสดออนไลน์ บนเว็บ UFABET

Replyhttp://ufabetvip.net/

http://ufabettip.net/

MyBlogger Club

ReplyGuest Posting Site

Best Guest Blogging Site

Guest Blogger

Guest Blogging Site

You can read interesting articles at this link.

Replyhttp://drpepperstarcenter.com/

http://kentrylee.com/

เควิน-เดอ-บรอยน์-บาทเจ็บ

Replyสูตรแทงหวยยี่กี"

Replyหงส์เซง-สื่อเผย-เฮนเดอร์สัน

Replyจุดอ่อนบาคาร่า

Replyพนันบอล

Replyแทงบอล 888

The leading casino web site welcomes those who are interested, click here.

Replyสล็อต ออนไลน์

เว็บ หวย ออนไลน์

เลขเด็ด หวยออนไลน์

หวยฮานอย

ตารางสูตรบาคาร่าฟรี

Replyบาคาร่าออนไลน์

Replyพนันบอลออนไลน์

เว็บบอลออนไลน์ สมัครฟรี

ReplyUFABET รวม คาสิโน ชั้นนำ

สมัครคาสิโน

Replyเว็บคาสิโน เซ็กซี่บาคาร่า

Suggest good information in this message, click here.

Replyตารางบอล

แทงบอล ออนไลน์

Welcome to the online gambling website. online casino

Replyufabet com

หวยออนไลน์

Let us take care of the experience Your best online casino

Replyบาคาร่า เล่นง่าย

บาคาร่าฟรี

ป๊อกเด้ง ทำเงินได้จริง

เว็บแทงหวย

แชร์สูตรเล่นสล็อต

สูตรเล่นรูเล็ต

เกมสล็อต เว็บเดียวจบ

Let us take care of the experience Your best online casino

Replyบาคาร่า เล่นง่าย

บาคาร่าฟรี

ป๊อกเด้ง ทำเงินได้จริง

เว็บแทงหวย

แชร์สูตรเล่นสล็อต

สูตรเล่นรูเล็ต

เกมสล็อต เว็บเดียวจบ

UFABET AUTO ระบบออโต้ ปลอดภัย รวดเร็ว

Replyufabet เกมพนันที่คนเล่นเยอะที่สุด

วิธีการเล่นบาคาร่าออนไลน์ ufabet

เกมยิงปลาออนไลน์ sbobet

โปรโมชั่นการเล่นพนันออนไลน์ ufabet

รูเล็ตออนไลน์ เล่นยังไง

ทดลองเล่นเกมยิงปลาออนไลน์

การพนันออนไลน์ น้ำเต้าปูปลาที่ได้เงิน

เกมยิงปลาออนไลน์ ยิงไว ตายไว 918 kiss

เล่นรูเล็ตออนไลน์ ให้ได้เงิน

online gambling website all bets Online Games Make Money >>> Click Here

Replyเกมยิงปลา Ufabet

แทงบอล ปป

Many different types of betting games Sign up click here

Replyเกมรูเล็ตคืออะไร

สล็อตเครดิตฟรี

สล็อตออนไลน์ มือถือ

หวยออนไลน์กับเว็บหวยsiam lotto

I think this is the best blog for you.

Replyคาสิโนออนไลน์ ไม่ต้องทําเทิร์น

คาสิโนออนไลน์ ได้เงินจริง แจกเครดิตฟรี 2020

แทงบอล 888

ราคาแทงบอล

คาสิโนออนไลน์มือถือ

เล่นบาคาร่าออนไลน์ฟรี

บาคาร่า พันทิป

โหลดบาคาร่าออนไลน์

สล็อตออนไลน์ มือถือ

คาสิโนออนไลน์ ที่ดีที่สุด

แทงบอล ufabet

Replydifferent game formats that can choose to play as they want

Replyหวยออนไลน์

บาคาร่า ออนไลน์ มือถือ

บาคาร่าเครดิตฟรี

สล็อตpg ค่ายสล็อตอันดับหนึ่ง

Replyกติกา ป๊อกเด้ง ออนไลน์แบบมาตรฐาน

ราคาบอล ufabet ออนไลน์

Suggest good information in this message, click here.

Replyป๊อกเด้งออนไลน์ ได้เงินจริง

ป๊อกเด้ง กติกา เล่นง่าย ทำเงินไว

PGSlot ค่าเกมดังมาแรง บริการ 24 ชั่วโมง

ยี่กีสูตรเครื่องคิดเลข

Replyสูตรเสือมังกรปอยเปต

สูตร รูเล็ตขั้นเทพ

These chapters are the most useful, able to help you calculate anything.

Replyเกมยิงปลาได้เงินจริง

เกมยิงปลาเว็บไหนดี

เกมยิงปลาฟรี

เกมยิงปลาเล่นยังไง

เกมยิงปลา pantip

ufabet ทางเข้าเล่น

ufabet ทางเข้า888

ทางเข้า ufabet

ทางเข้า ufabet มือถือ

ทางเข้า ufabet1688

สูตรเล่น เสือมังกร ที่ทำเงินได้ดี

Replyเสือมังกร ออนไลน์

เสือมังกร ออนไลน์

เกมป๊อกเด้งออนไลน์

น้ำเต้าปูปลา

ซื้อ หวยออนไลน์

ซื้อ หวยออนไลน์ บาทละ 900

ซื้อหวยออนไลน์เว็บไหนดี

เว็บหวย

คาสิโนออนไลน์อันดับ-1

Replyคาสิโโน-เว็บตรง

สล็อต-xo-เครดิตฟรี

A good website is useful.

Replygame sbobet

บาคาร่าคือ

แทงบอล เว็บไหนดี

แทงบอล เว็บไหนดี pantip

A good website is useful.

Replyเกมคาสิโนในระบบออนไลน์

คาสิโน ออนไลน์

เว็บพนันที่ดีที่สุด

คาสิโนออนไลน์ เว็บตรง

เว็บพนันออนไลน์

thank you for introduce and good product

Replyเว็บ แทง บอล ไม่มี ขั้น ต่ํา

UFABET เว็บตรง

แทง บอล ชุด

สมัคร ufabet

ป๊อกเด้งออนไลน์ขั้นต่ำ1บาท

Ways to make a profit from online gambling sites.

Replyทางเข้า UFABET

ufabet 111

ufabet kick

เว็บแทงบอลผ่านมือถือ

มือใหม่ แทงบอลออนไลน์

Thank you for your interest.

คาสิโนออนไลน์

Replyราศีที่ต้องระวังพบรักหลอกลวง บนโซเชียล

French Kitsch Project คาเฟ่ที่ชิค และบรรยากาศดี ของเมืองโคราช

The Royal Treatment ยัยสาวตัวร้ายกับเจ้าชายจอมมึน

คาสิโนออนไลน์

Replyเผยเคล็ดลับ ไหว้เทพเจ้าไฉ่ซิงเอี๊ย เสริมโชคลาภ ตรุษจีนนี้

"ฉ่อย" เป็ดย่างร้านระดับตำนาน กับรูปแบบเดลิเวอรี่

Single All the Way หนังรักโรแมนติก LGBTQ

คาสิโนออนไลน์

Replyฝันเห็นระฆัง ฝันว่าได้ยินเสียงระฆัง

Moonfall วันวิบัติ จันทร์ถล่มโลก นับถอยหลังสู่วันสิ้นโลก

สูตรแทงบอลสูงต่ํา

Replyวิธีแทงบอลออนไลน์

ตารางบาคาร่า

บอลสเต็ปออนไลน์

ufajom.xyz

บาคาร่าสด

แทงบอลออนไลน์

ReplyUFABET คาสิโนออนไลน์ ชั้นนำ ครบวงจร

วิธีเล่นบาคาร่าเบื้องต้น

หวยออนไลน์ จ่ายจริงไม่มีโกง

ค่ายเกมสล็อต

Replyเว็บบาคาร่า อันดับ 1

เสือมังกร ออนไลน์ 10 บาท

รีวิวเกมสล็อต Roma X

คาสิโนออนไลน์

Content as desired Thanks for the good story

thanks for the content and useful stories

Replyหวยรัฐบาล

ดูบอลสด

slotxo

รีวิวบาคาร่า

รีวิว

This article will help raise money for everyone .

Replyรีวิว

slotxo

บาคาร่าgdg

แทงบอลสเต็ป

เลขเด็ด

Thank you for your support

Thank you for your info it's helpful for me

Replyรีวิวแฟชั่น

บาคาร่าเล่นยังไง

ตารางบอล

ตารางหวย

สล็อต

Thank you for your info it's helpful for me

Replyรีวิวอุปกรณ์กีฬา

สมัครเว็บพนันบาคาร่า

แทงบอล-สูง-ต่ำ

หวยรัฐบาล-เล่นยังไง

ufaslot

Your information it's very helpful Thx.

Replyรีวิว

slotxo

บาคาร่าgdg

แทงบอลสเต็ป

เลขเด็ด

joker gaming

Replyสล็อตเว็บตรง

ทำไมต้องเล่น 789gashaslot

ดูหนังออนไลน์ฟรีNormally I do not read article on blogs, but I would like to

Replysay that this write-up very compelled me to take

a look at and do it! Your writing style has been surprised me.

Thank you, very great article.

ดูหนังออนไลน์ใหม่2022ดูหนังออนไลน์2022

ReplyThank you for writing an interesting message. make me recover from boredom Please come and visit my blog. ดูซีรี่ย์ออนไลน์

Reply