Don’t ever let anyone tell you this business isn’t hard. If it wasn’t, everyone would do it. Making investment decisions with millions of dollars is not only hard work, it is by definition stressful.

I remember a colleague once saying he took pride in making money for the school teachers and pensioners that were the main investors in the fund. That's laudable, yet it works both ways--when you go through the inevitable slump where you lose money on a seemingly unending basis, you get this feeling in the pit of your stomach that you’re letting down the teachers, letting down your family, and hmmm, maybe both of them are going to hire someone else for the job if you don’t get your act together.

As much fun as it is to look at someone else’s investment recommendations and laugh at their ineptness with the benefit of hindsight, I sympathize. It’s not easy to put yourself on the line and publish your top six trades for 2017 as the folks at Goldman Sachs so kindly did last November. While you might read a little snarkiness in the following piece, it is with the utmost professional respect!

With those disclaimers out of the way, let’s go into the time machine, back to the days when the US had just elected a fresh faced new president had just been elected and the country was brimming with hope and optimism.

Alright, maybe not so much. Trump voters were gloating, Hillary supporters were weeping, and bond investors were running around like their pants were on fire. British voters were some combination of all three. And the Germans were tut-tutting. With that context..on your marks, get set….

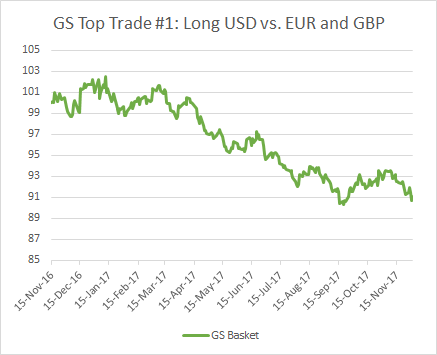

Top Trade #1: Transatlantic economic divergences and political risks Long US$ equally weighted against EUR and GBP, with a basket indexed to 100, a target of 110 and a stop at 95. Annual carry on this basket is 1.3%.

Uff. Not off to a great start here. Stop City. I’ll say this….the stop at 95 was good trading discipline.

What went wrong? The idea was two fold: 1) The US economy would continue to grow strongly, and 2) The European economy would stagnate, which would combine with political risk on the continent and in Britain to torpedo EUR and GBP. Amazingly, they got #1 right….and they weren’t wrong about political risk in the UK...but that didn’t matter when the economy started to grow. This caught the entire currency market off guard, which had grown so accustomed to using EUR as a funding currency it didn’t occur to them that Europe still possessed 1) a business cycle and 2) an amazingly efficient German export machine.

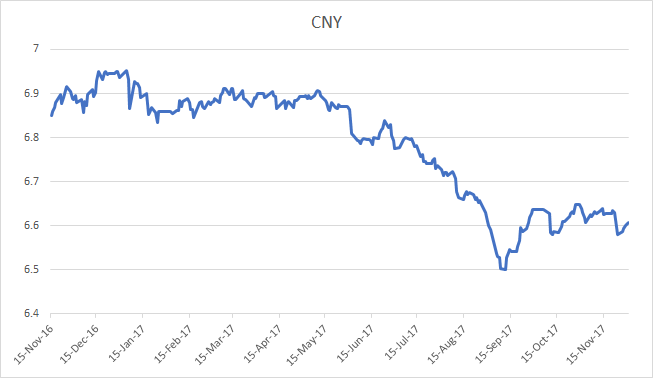

Top Trade #2: RMB weakening: Long $/CNY Long $/CNY via the 12-month NDF, currently at 7.07, for an initial target of 7.30 with a stop at 6.75.

Ouch. Stop City again. But that Stop discipline REALLY worked this time! Putting in that stop ticket to sell usd/cny at 6.75 felt so, so bad….but it was so, so good. Sometimes the best trade you make is the stop loss!

Here was the thesis, in a nutshell:

"The fundamental dilemma of China’s currency regime is that, in an environment of a rising dollar, keeping the CFETS basket stable requires $/CNY to move higher meaningfully, which carries the risk that capital outflows re-escalate," the team writes. "Our base case is one where the $/CNY fix continues to grind higher, driven by domestic pressures and in the context of a stronger dollar."

What went wrong? 1) The dollar didn’t rise. In fact, quite the opposite. 2) They assumed a risk that capital outflows could, and would re-escalate owing to domestic pressures. Wrong again...local capital outflows subsided notably and there was zero pressure on FX reserves all year. Interesting to note here they missed the most ubiquitous China theme of 2017: Stability in anticipation of the 19th National Congress of the Communist Party in October. For most of Q2 and Q3, you couldn’t swing a dead cat without hitting three analysts telling you the government was doing everything in its power to maintain control over markets and vol until the Congress was behind them. That didn’t even bear a mention...the lesson: narratives can change quickly, even when news doesn’t.

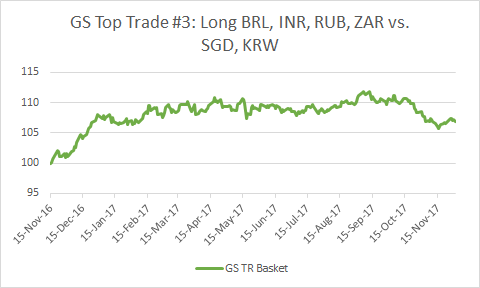

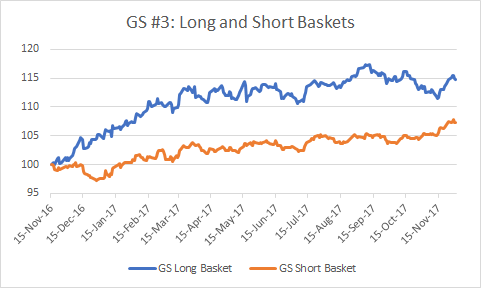

Top Trade #3: Earning the ‘good carry’ in EM, hedging the China (and CNY) risk Long an equally-weighted basket of BRL, RUB, INR, ZAR versus short an equally-weighted basket of KRW and SGD, with an entry level of 100, total return target of 114 and stops at 93. The expected return, including approximately 7% carry (on an annual basis) and 7% price return, is around 14%.

Here’s one that worked...the basket didn’t quite reach the 114 target but we’ll take it! The story here is all of these currencies did reasonably well...so while successful this is more of a beta story rather than alpha.

INR and RUB could be considered “good carry” in 2017, as India benefited from strong growth and improved productivity and RUB took advantage of the weak USD and higher oil prices. BRL and ZAR turned in decent performances, thanks in no small part to hefty carry, but they left you with more than one sleepless night. The core theme was right--long high-beta EMFX funded by low-beta/low-rate Asian exporters. Nice trade. So let’s not split hairs here...we’ll chalk this one up as a W!

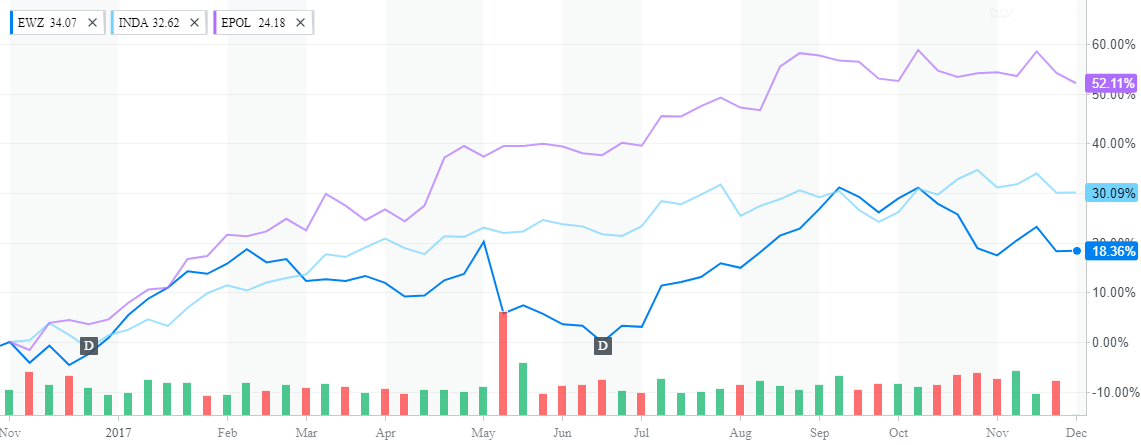

Top Trade #4: Long EM equities with insulated exposure to growth Long Brazil, India and Poland equities (BOVESPA, NIFTY, WIG) FX-unhedged, with an entry level of 100, for a target return of 120 and a stop of 90.

Nothing to even discuss here--this trade crushed it out of the park. The chart above uses the iShares ETFs for each country as a proxy for the local index FX-unhedged. Great work, Goldman Equity Guy!

Top Trade #5: The ‘reflation’ theme extends and broadens Long US 10-year US TIPS ‘break-even’ inflation at an entry level of 1.90%, with an initial target of 2.30% and stop at 1.60%, and long Euro 10-year inflation via swaps at an entry level of 1.25%, with a target of 1.60% and a stop at 1.00%.

We’ll give credit on this one too...I mean really, paying inflation in 2017!?! You had already missed the “easy money” in this trade after inflation breakevens ground higher from historic lows in mid-2016. Then the US election bear steepened global curves and moved BEIs materially higher. Then Goldman comes out and says “don’t stop now...we’re just getting started...” On a theme that hadn’t worked consistently in at least a decade.

I’ll give full points for degrees of difficulty here--In 10y TIPS….paying at 1.90% was a momentum trade last November that looked absurd by the summer as one inflation print after another came in below expectations. But it has come back to within spitting distance of the entry point as some big investors have paid up for inflation protection in size, as we discussed here last week.

The 10y EUR swap trade hasn’t quite gotten to to the 1.60% but we may get there by year end...and even if we don’t, a 30bps move is a spicy pickup in that space. Was stronger growth part of the elixir? Not really, but sometimes the trade works for the wrong reason, and we don’t argue.

Top Trade #6: Long equity-like ‘carry’ with little duration risk through dividends: Long EURO STOXX 50 2018 dividends Long EURO STOXX 50 2018 dividends (BBG: DEDZ8 Index) equity-like ‘carry’ with little duration risk; target 125, now at 112 (12% unfunded return), stop at 105.

I’m not sure what this one means. Dividends probably had a good year, thanks to continued low rates, strong profit growth, and good equity returns. If someone wants to send me the DEDZ8 chart, I’ll post it, but I’m just going to say it probably had a decent run and move on with my life.

So there it is...two dead wrong, “why, oh why did I do that” stop losses (#1, #2). two doubles into the gap (#3, and #6 which I’m willing to amend this upon further evidence), a clean single (#5), and a three-run bomb to deep center (#4).

Make no mistake...what you see above a pretty good slugging average, especially coming off of 2016 when these guys got carried out of four trades before January was over. Can they do it again in 2018? Stay tuned, we’ll go through Goldman’s top ideas for 2018 tomorrow.

12 comments

Click here for commentsEither its a 1)"let he without sin cast the first stone" or 2)peeps are still calculating if the six trades outperformed spooz.

ReplyAlas I 1)Can't and 2)didn't outperform spooz(by much).

Well, that brings up a good point, I didn't bother with benchmarking since I think goldman's client base are mostly thinking absolute return.

ReplyYou're probably right about #2, but only because the financial media obsesses with the performance relative to the S&P. Every article on bloomberg about (usually poor) hedge fund performance is obligated to compare the returns to the S&P, when no hedge fund in the world has the S&P as a stated benchmark...because then it would cease to be a hedge fund!! One would think the bright people writing these articles would be able to understand basic concepts of duration....macro/RV/FX + leverage = short duration = benchmark is spread over LIBOR. Fixed income + some or no leverage = bond benchmark. Equity + low or no leverage = really long duration = equity benchmark.

This package has 2 equity trades, 3 FX trades, and 1 (short) bond trade. Reasonable benchmarks are: Equity 24% (total international equity return), FX +6% (performance of FX vs. USD this year), Bonds +3% (international total bond return...clipping coupons), and LIBOR +1%.

The pol/bzl/india equity trade clocks in at something like 33% return, so there is some healthy alpha above plain vanilla equity returns there, even if some of that is attributable to FX (a binary risk they explicitly took on). The inflation trade is a LIBOR benchmark, which is a success. The FX trades as a package are a bust by any measure. And the "dividend" trade is still too opaque to assess...

1-year ahead predictions are tough (except for long equities, of course). Willing to cut these guys some slack, as you do.

ReplyInteresting reversal in the Russell. All those small-mid-caps are sell-the-news trading sardines apparently.

Any views on South African long bonds here?

Where did the morning screaming rally go? :-) Noticeable that the R2k reversed on the day, so did the short vol ETFs, and so did USDJPY. Not what would have predicted at 4am after waking with the usual sense of foreboding to see the futures up 10 handles.

ReplyLB remains long yen, short Nikkei, on what began as a purely technical trade - and now finally has some company at last:

http://www.zerohedge.com/news/2017-12-04/buying-yen-truly-contrarian-call

We didn't have any Japanese fundamentals like this to discuss when we called it a few weeks ago, the yen reversed to a slightly higher RSI, because everyone was already short and suddenly it just WASN'T GOING DOWN ANY MORE.

I liked the macro tourist piece. Not sure I agree, but I really liked the approach, and can see where that is going to take off like a rocket when/if the BoJ takes their foot off the pedal. I just don't see it happening soon. I dug into the flows after reading the piece, the rally in stocks amid the stability in JPY has been a function of locals slowing down or reversing capital flight, while the BoJ has been pounding the offer in stocks.

Reply@Johno re: South Africa, benchmark bonds look cheap here, I guess this ratings talk has people scared out of the water--but lets face it, this is yet another winter of our discontent as years of fiscal ineptitude finally catches up with the government. The curve looks too steep to me given inflation risks and simply not enough carry in ZAR to stabilize volatility when the ship starts listing. I can't get outright long there without a compelling catalyst for how the Zumas are out of office or into exile, or without even a widely supported fiscal reform plan. But I like flatteners or long duration + long usd/zar, which seems to have gotten out ahead of rates. That's a 30k foot view...what do you think?

ReplyYes, I think long bonds are far more interesting than the currency and agree, if there's a trade here, it's long duration + long usdzar. I'm perhaps missing the trade as I'm not sure how the ANC leadership race pans out, even with the branch nominations favoring Ramaphosa.

Replythe thing is, even if Ramaphosa wins, the Zumas don't just leave town. It could turn into a power struggle rather than the beginning of a reform movement. It would be a step int he right direction though.

ReplyWe didn't have any Japanese fundamentals like this to discuss when we called it a few weeks ago, the yen reversed to a slightly higher RSI, because everyone was already short and suddenly it just WASN'T GOING DOWN ANY MORE.

Replygoldenslot

สล็อตออนไลน์

สมัคร gclub

31AxRDv

Replyفروشگاه لوازم آشپزخانه نارنجی

ghazabarghi

ظرف غذای برقی

profile-138531

دانلود فول آلبوم آرون افشار با لینک مستقیم

فرش مسجد

Replyفرش سجاده ای

تابلو فرش چهره

Ayo guys daftar idn poker di agen idn slot online terpercaya hanya di vtgplay.com bukan di tempat lain ya :)

Reply