Maybe it's just always been too far afield for me, but I think the Japanese yen is the death star of macro trading. There are a vast number of variables that don’t really apply to other FX markets, and your positions exists at the pleasure of the BoJ, which has the power to open fire with this “fully armed and operational battle station” to destroy whatever planet you are living and trading on. And if that’s not enough, it is the funding currency of all funding currencies. So go ahead, spit into that gale force wind.

But I just can’t shake JPY...and the possibility it makes a big move stronger this year. In the comment section from last week’s post Johno asked the big question for JPY in 2018:

One question concerning USDJPY I may have posed before is what happens if we get inflation >1% in Japan. Some argue that YCC will remain, or slowly adjust, pushing real rates down and with it the currency. Others argue markets will look forward, anticipating removal of YCC, higher rates, and pushing the currency stronger.

I’m in the latter camp. Here’s why. There are a confluence of factors that are pushing the yen towards strengthening.

The economy is picking up in a way that hasn’t occurred in many, many years. I can bombard you with charts on this one, but I found this one to be particularly telling. Credit growth is picking up, and rising significantly while it is flatlining or decelerating in Europe and the United States.

That says to me that there are good investment opportunities in Japan, and now that there are signs global growth might support an increase in export capacity, businesses (both foreign and domestic) are starting to take advantage of that. That might be the beginning of a turn from a very large industrial battleship.

The economy is picking up in a way that hasn’t occurred in many, many years. I can bombard you with charts on this one, but I found this one to be particularly telling. Credit growth is picking up, and rising significantly while it is flatlining or decelerating in Europe and the United States.

That says to me that there are good investment opportunities in Japan, and now that there are signs global growth might support an increase in export capacity, businesses (both foreign and domestic) are starting to take advantage of that. That might be the beginning of a turn from a very large industrial battleship.

Second, the Yen is cheap. Really cheap. MacroTourist started me thinking along this line a few weeks ago, and I guess I’ll just put my spin on what he said:

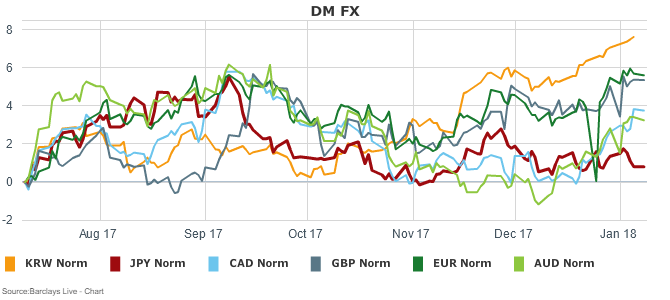

JPY has been left behind by every other DM currency in the great USD-fire sale of 2017:

Including against KRW, which has appreciated markedly as the BoK has taken its foot off the intervention pedal, and amazingly, moved to finally hike rates. Tough to envision a break of 9.00 here now that the Korean government is calling time on the strong won.

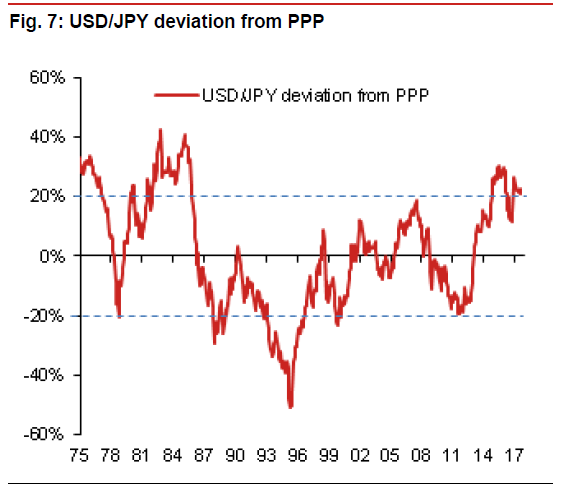

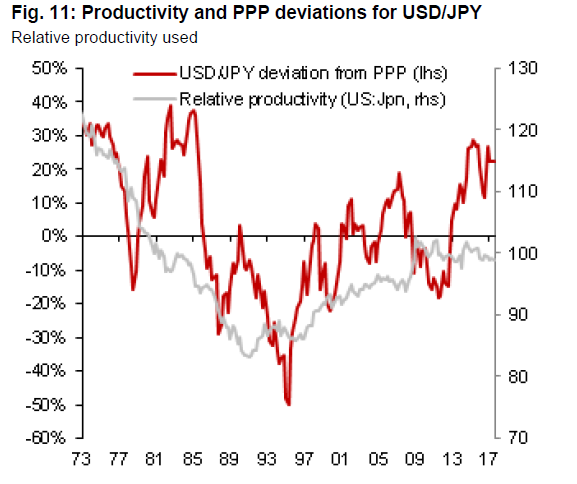

That’s nominal rates...but real rates, or purchasing power parity valuation, show an even more attractive picture. USD is roughly 20% rich to JPY on a PPP basis.

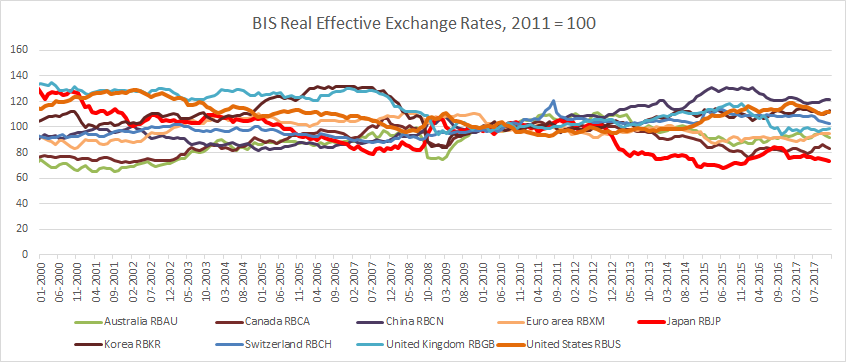

And as I have noted in the past (repeatedly, I’m afraid) the BIS real effective exchange rates shows the yen skulking at the bottom of the table for DM FX:

All this, despite the fact there is little evidence of a breakdown in the relative productivity of the Japanese and US economies:

Right...so some mysterious force….the dark side, the light side….we don’t know which...is sandbagging the yen. What could it be?

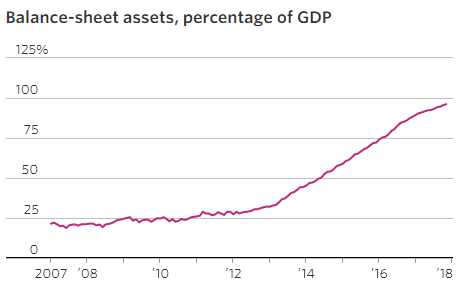

Yep, it’s this....The BoJ's printing press:

I could argue until I’m blue in the face that a chart like that can’t go on forever--but maybe it could! This gets back to the crux of Johno’s point--will the BoJ keep the pedal to the metal, or will the market price in an easing of this reality TV episode of “The World’s Most Extreme Central Bankers”? If you poke around the street and “fintwit”, various forces will argue that there is already a “stealth taper” from the BoJ. If you look at their total assets, that might be true, but without any official word from Kuroda and Co., it is hard for me to trade on that.

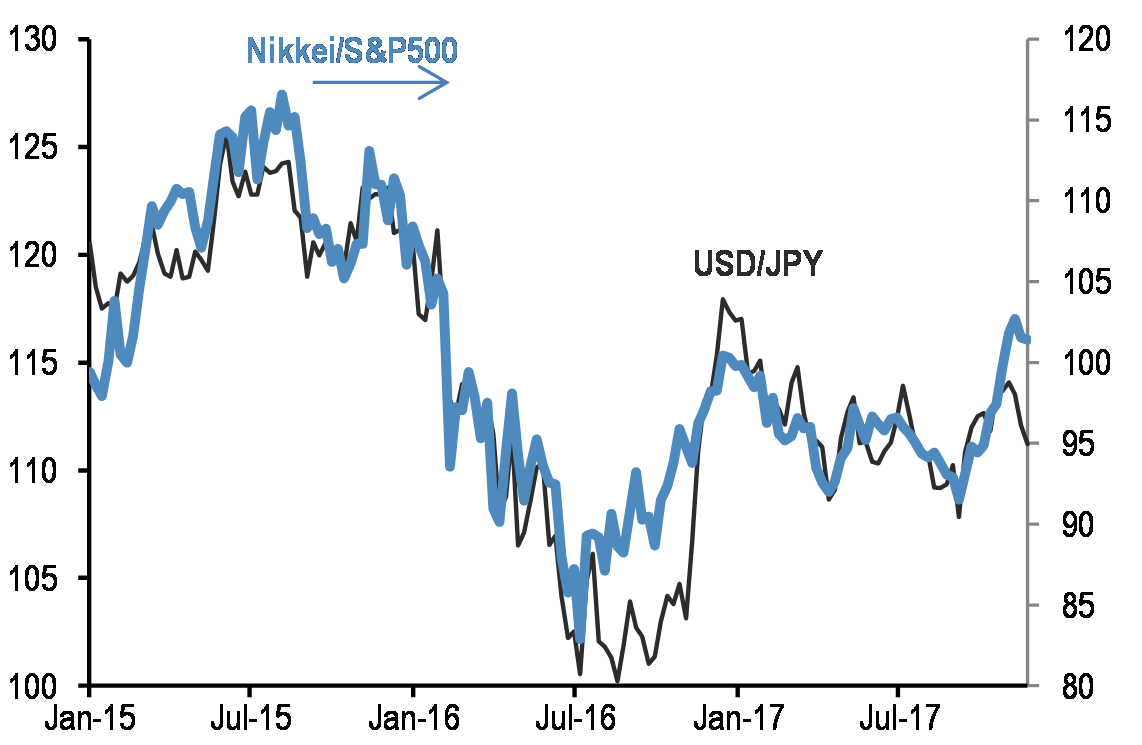

Many will point to the correlation between stocks and JPY. This correlation raced towards 1 when Abenomics took off in 2013. That correlation has broken down lately as optimism on the economy and foreign and domestic flows have led the Nikkei to outperform USD/JPY.

Will this relationship mean revert? I guess it could, one of two ways: 1) FTQ….stocks could take a big dump on any number of risk factors. The newly high-beta Nikkei cools off while USD/JPY grinds lower, or 2) Kuroda pulls out the Draghi card and says he’s still going to do “whatever it takes” to reinflate the economy, and the YCC target isn’t going anywhere. The former is a random variable (and positive for long JPY anyway)...the later is possible, I just don’t see it happening.

I think the market will eventually price an easing of the YCC policy more broadly than they do now. Importantly, the odds aren’t “even”...despite accelerating domestic growth, the yen is still the currency traders love to hate.

That leads us to the technicals. Locals are starting to reverse a long period of fleeing local markets in favor of foreign bonds...I can’t find a clean data set showing the history here but the potential repatriation inflow from domestic investors that have fled Japan in favor of foreign markets is massive. If this flow even tips towards balance, it would be hugely supportive for JPY.

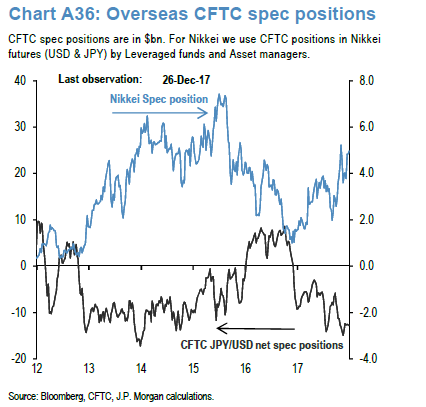

Moving to the dark art of CTFC FX spec positioning...despite signs of life across all sectors of the Japanese economy, the short yen position is at a multi-year extreme:

And we remember from 2017 what can happen when the story “flips” in a currency with an extreme and structural short position:

Currencies are a zero-sum game (in DM, anyway)....but here the odds aren’t even. You’re getting good terms to take JPY risk here.

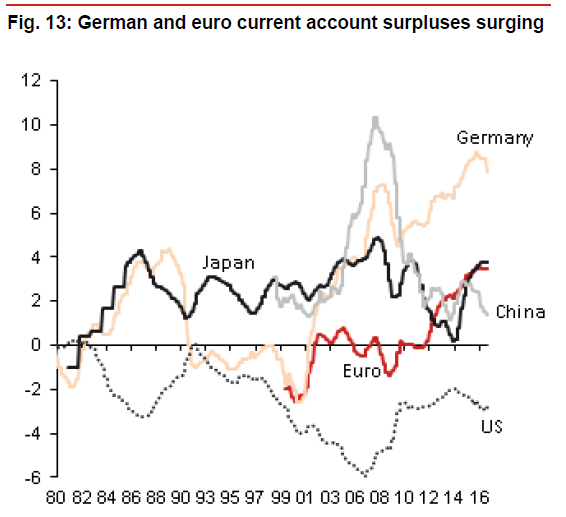

Lastly, there is the tailwind from the dollar and capital flows. After the combination of dormant domestic demand, the Fukushima earthquake, and high oil and food prices crushed the current account early in this decade, the surplus is back, baby!

Just as important, as the American consumer has picked up some speed, the US c/a deficit has started to turn lower again. Historical evidence suggests that the combination of a rising surplus in Japan and a deficit of 2.5% or higher in the US is a negative signal for the dollar.

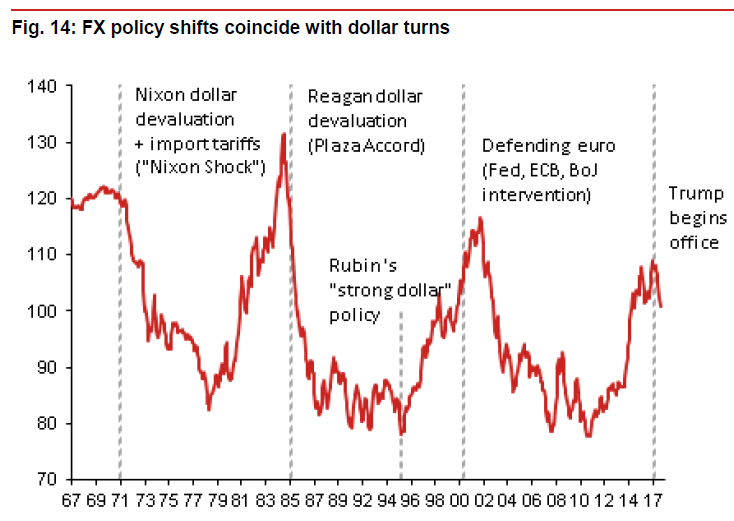

And indeed, as I noted last week and IPA will be glad to tell us again, there is significant air beneath the dollar here, even after the poor performance in 2017.

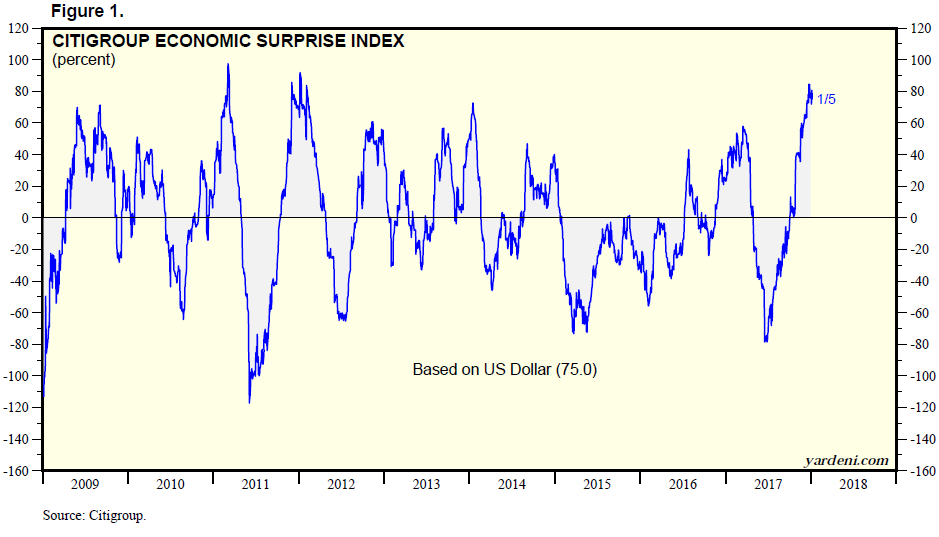

And just as an aside, despite my misgivings last fall, I don’t see the structural support for an acceleration in inflation that will trigger a more aggressive hiking cycle, and subsequent USD appreciation--from the FOMC. Nor do I buy into the policy-driven growth renaissance in the US. The economic surprise index tells me there is more downside than upside there, too.

Putting it all together as we like to say….cheap valuations, attractive positioning, strong fundamentals and potential for positive surprises from both sides of the trade (monetary in Japan, economic in the US) makes for an attractive risk-reward in buying yen.

There it is. The first case I’ve ever made to buy yen. Deflector shields are down, blast away.

36 comments

Click here for commentsCouldn't agree more, and I think the correlation trade johno mentioned (against the US Ten Year) is the most interesting way to play it. That said, I love having Yen (outright) in the portfolio as a hedge against my risk-on positions. Options might be interesting too.

Reply... "There it is. The first case I’ve ever made to buy yen. Deflector shields are down, blast away."

ReplyPerhaps, the case you make to buy the YEN is against the wrong currency. Just saying...

I thought about making a case for crosses--certainly makes sense as well. Just by chance I believe MM's bbg column yesterday was on that subject. The technical positioning argument is strong for short eur/jpy, but less so the fundamentals and valuation, in my opinion. That said, as I alluded to with the surprise index, one could say expectations are similarly too far over their skis in Europe as well.

ReplyAgreed. Like EURJPY short best, or perhaps short AUDJPY.

ReplyAlready have a small position short USDJPY. It is perhaps the best apocalypse hedge of all, per William B above. Better than gold, for example in a total meltdown, which would result in a massive yen carry unwind (see 2008). Shorting the inverse vol vehicles is another apocalypse hedge but you're more likely to be destroyed waiting, hence the utility of options here.

Death of Bond noise us deafening again in the media, expect more of that until another tame round of inflation data. Yawn....

If we start seeing the USDJPY ~ 10Y correlation breaking down, I'd imagine it would be USDJPY bearish as all the longs using it as a proxy for the 10Y would have to exit (after all, what's the point of a trade that doesn't work when it's supposed to, and exposes you to massive downside if the risk regime flips negative?). Today's action couldn't have made the USDJPY bulls happy ...

ReplyChange to the CNY fixing regime was probably most significant news item today. Second time USDCNY gets to 6.50 and China changes the rules to support. Suggest to me the USD/Asia fall at least takes a breather here.

Beginning of the year a tough time. Easy to make FOMO mistakes. I already made one buying some EURUSD calls with spot above 1.20.

Yeah i think the PBOC move was the second brick in the wall after the govt tried to take some steam out of KRW on Monday. should be yen positive on the margin--although it will take more force than this to clear out long asia/short jpy carry trades.

ReplyReally interesting piece but the correlation stuff between S&P500 and USDJPY may be exaggerated ? I mean, if you go back 10 years, correlation between the two stands at 0.7125 but if we go back to just 2017, last year correlation was -0.03.

ReplyI can't shake the jonah in 12 Yarra Burra street ,Gymea.

ReplyI'm tipping your jonah is around a lot longer than mine.

ReplyI'm still here, pal. Ass in tact.

ReplyA map to the worlds greatest Jonah ever to not step into a betting ring.

Replyhttps://www.google.com.au/maps/place/12+Yarra+Burra+St,+Gymea+Bay+NSW+2227/@-34.0503809,151.0784311,17z/data=!3m1!4b1!4m5!3m4!1s0x6b12c7100ad3487b:0x9c7e9391d9452ace!8m2!3d-34.0503809!4d151.0806198

And let's all keep it that way!

ReplyMacro Man, pal. The only way your walking in the betting ring with a tip sheet is on a quadruple-triplet snowman.

ReplyHi this is good to see that you are providing such great service and you giveing it for free. I love type of blogs that understand the value of providing a quality information. Thanks for sharing it very useful for Help Adya Used Clothes Online in India. www.helpadya.com

ReplyI tell you what , Macro Man pal. If the whitewalker comes to my door step and ask personally for my tipping service, I'll promise to yield the knee.

ReplyBetter still, pal. You come!

ReplyC**t

ReplyF**kin C##T

ReplyLet's trade one on one , Macro Man pal.

ReplyLet's trade one on one , pal. By the river , on the diamond , where south faces north. C##T.

ReplyOooo, correlation breakdown getting nasty. Flee, flee, USDJPY shorts!

ReplyWell-timed piece, Shawn!

Scapino: we're talking about US 10Y versus USDJPY, not SPX.

Replythere's johno. Guess what , johno. I'm still visiting the joy houses. Think about it. C##T.

We thank the BoJ and the unnamed Chinese sources for the unexpected yen spike, we cashed that one in for now, but as we have discussed above, stronger JPY may be a theme worth returning to.

ReplyAnother Death of Bond week, as we and others had predicted. We bought some TLT calls first thing today. Already this morning, yields have fallen a bit from the highs, and we expect that to continue with the "red-hot inflation data" due to be released this week… yawn!

Bill Gross is now short Treasuries, btw, but Bill, so is everyone and their Uncle, already. PIMCO are adding, Bill, and, get this: they are BIGGER THAN YOU ARE. Just sayin'…

Btw, all is not well in credit markets, although some clowns are saying we are in "mid-cycle" in credit, the data for C&I lending and bankruptcies tell a different story. The carnage in retail is well known but it's not necessarily "contained", and there are signs that things are getting ugly. Maybe we are late cycle and the MSM didn't notice this yet, then again, perhaps this is to be expected. "It gets late early this time of the year", as someone said.

https://snakeholelounge.wordpress.com/2018/01/09/chapter-11-filings-soar-ci-lending-growth-stalls-unpeaceful-uneasy-feeling/

As is always the case, the sheer size of the credit markets and the illiquid nature of many high yield offerings dictates that the rush for the exits is likely to be disorderly when it begins. Treasuries will be the beneficiary of any repricing of risk in US credit markets...

Vol watchers may have noted VIX and Spoos rising together M and Tu, that's invariably a sign of "irrational exuberance" and FOMO - tiny punters are call buying, put/call ratios are at very low levels. These are not usually good short-term signs for Mr Market as we await the latest round of earnings and other corporate fantasies. Watch the banks and the FANGs closely. Breadth has been declining for a while - if and when the leaders turn south things will get interesting in a hurry.

there's leftback pal. No stiches in my ass this week from the market , pal. But , don't tell the silver spoons. They want me walking around bandy legged by the time they come around asking for tips.

ReplyLB,

ReplyI think the thing that would concern me right now about being short bonds is that the Spoos in terms of bullish percent are more extended than they have been for at least several years. Tends to imply there isn't a lot more breadth to be had in US risk and typically if profit taking sets in then treasuries are likely to squeeze shorts. That's not got much to do with the longer term picture of course ,but as we stand until some froth comes off US equities I'd be loath to be short bonds.

there's checkmate pal. Dishing out the rule of law about USA treasuries. Hat tip. When Wall Street is directing the plebs on main street how to inbreed the wildlings beyond the wall, you know where in a froth and bubble market.

Reply@johno : my bad, thx for the info

Reply@checkmate: you missed the irony implicit in my post… I should have written "Death of Bonds" like this, no?

ReplyIn case anyone missed it, there was a stonking demand for US10y at yesterday's auction, including uh, foreign bidders, which likely includes China… so apparently they are still interested after all!

Come to think of it, if I was China, would I reduce my Tsy holdings with yields at or perhaps close to a local maximum (i.e lower prices)? Or might I wait until there is a credit panic and yields fall to a low point (high prices)? This isn't rocket science….

No, I understood your view on bonds. It's been as unchanging as mine. I was simply saying why I would not choose to be short US bonds. As for China , talk is cheap, but the reality is exactly where are the other large ,liquid markets that will mop up there trading balance with the rest of the world OR are they planning to give all up ? Suppose they could start buying up Zimbabwe by so many sq miles per annum now you know who as been retired.

ReplyF*ck macro - no-one in that space has produced alpha for years.

ReplyIn the real world, real traders like us are still heavily long equities. This trade has outperformed EVERY FUCKING YEAR for the last 9 years! What are you waiting for???????

Look, out of 8 trading days in 2018, we've seen 7/8 new all time highs in the S&P and every day has been positive! The S&P500 will reach 3k in a few more weeks, and likely at least double in the next few years. I can assure you that equities will NEVER see a meaningful decline again in our lifetimes. Why? Because sovereigns and CBs are monetizing their national debts RIGHT NOW by printing money and buying equities - and these cocksuckers will never stop.

The Dow Jones up +100 pts (nearly 0.5%) since my last post (above).

ReplyLook, just blindly buy US stock indexes every time I post and you'll produce double-digit returns each year. It really is that easy.

It looks like after a very successful backtest of 1,310 gold is ready to break out. 1,360 is next, imho.

Replywhy trade macro? Leverage.

Replyunleveraged? sorry to hear that. 25x leverage in FX and 50x in DM rates.

ReplyVery Good bro.

Replyดูหนังใหม่ 2021

รีวิวซีรี่ย์ใหม่